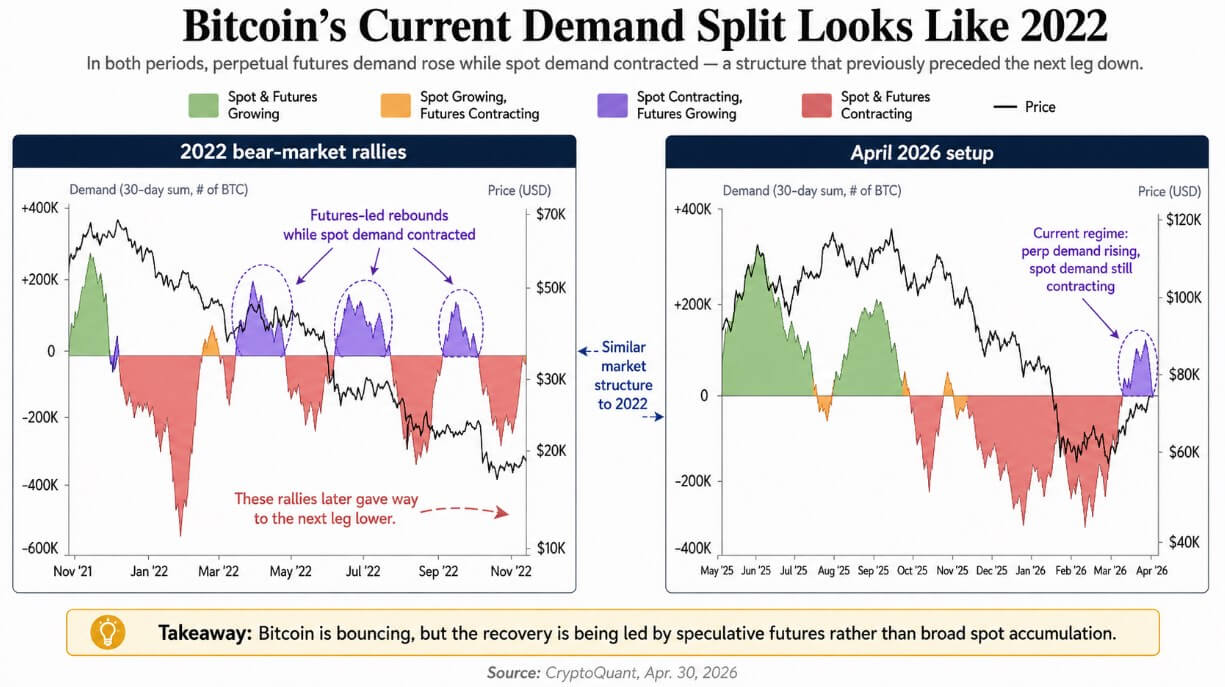

CryptoQuant’s newest Apr. 30 learn reveals that perpetual futures are driving Bitcoin’s restoration, whereas spot demand continues to be shrinking. That’s the similar market construction seen through the 2022 bear market rallies, when leverage-driven rebounds gave approach to contemporary draw back.

Spot shopping for via exchanges, ETFs, or direct on-chain accumulation represents dedicated capital. On the similar time, perpetual futures permit merchants to take directional publicity with borrowed capital, typically at multiples of their collateral, with out holding the underlying asset.

When each types of demand increase collectively, a rally tends to be self-reinforcing. When futures lead and spot lags, leveraged merchants finance the bounce and face pressured exits if the value strikes in opposition to them.

The 2022 comparability

A number of bear-market rallies in 2022 shared the identical regime, with perpetual futures demand recovering earlier than spot demand did. The value bounced, and leveraged positions got here off as spot patrons proved too skinny to soak up the promoting.

The bounces seemed constructive, however every one resolved into the subsequent leg decrease.

CryptoQuant’s chart locations Bitcoin’s present April 2026 transfer again right into a regime the place spot contracts are contracting whereas futures contracts are increasing. The parallel is that borrowed capital is reappearing earlier than actual money demand does, which is exactly the situation that made 2022’s failed rallies fragile.

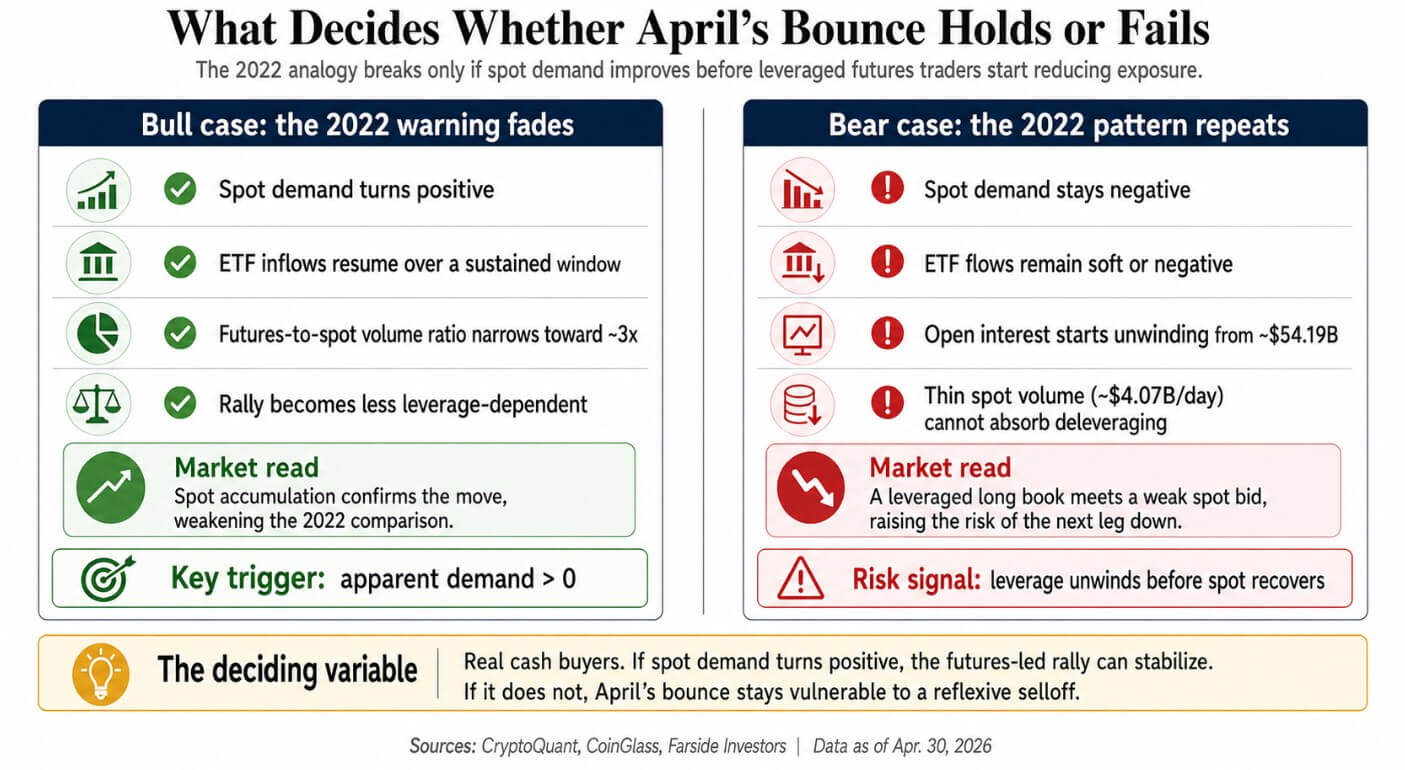

The dimensions of immediately’s futures market makes that fragility a bigger variable. CoinGlass information confirmed $47.64 billion in 24-hour Bitcoin futures quantity versus $4.07 billion in spot quantity, a ratio of about 11.7x, with open curiosity at roughly $54.19 billion as of Apr. 30.

Perpetual futures can contain borrowed capital as much as 50 instances the collateral on some platforms, which means comparatively small value strikes can set off giant pressured liquidations.

When spot quantity runs at $4 billion a day and a long-side flush begins, the market’s depth will get examined quick.

What the ETF information provides

US spot Bitcoin ETF flows have not too long ago strengthened the market construction warning, as Farside Buyers information reveals mixture outflows of $490.5 million between Apr. 27 and Apr. 29.

The ETF bid has gone uneven at precisely the second futures positioning is increasing, whereas the long-run ETF image holds its form.

| Metric | Present learn | Why it issues |

|---|---|---|

| BTC futures quantity, 24h | $47.64B | Derivatives exercise is dominating the market |

| BTC spot quantity, 24h | $4.07B | Spot help is way smaller than futures exercise |

| Futures/spot quantity ratio | 11.7x | Exhibits the rally is closely leverage-driven |

| BTC open curiosity | $54.19B | Massive leveraged place base that might unwind |

| US spot BTC ETF flows, Apr. 27–29 | -$490.5M | Latest ETF demand has turned uneven |

| IBIT cumulative web inflows | ~$65.2B | Lengthy-term institutional demand stays sturdy |

| Whole US spot BTC ETF cumulative inflows | ~$58.1B | The structural ETF bid continues to be optimistic total |

IBIT alone accounts for roughly $65.2 billion in cumulative web inflows, and the complete US spot Bitcoin ETF class totals about $58.1 billion, numbers that replicate real structural shopping for absent in 2022.

From Apr. 13 to Apr. 29, IBIT nonetheless absorbed about $1.47 billion in web inflows, conserving the longer-term institutional image intact. The near-term learn is that the ETF bid will not be at the moment offering clear help for value at a time when futures positioning would most want it.

The bull case

The 2022 analogy breaks when spot demand turns optimistic earlier than leveraged merchants begin decreasing publicity. CryptoQuant’s obvious demand measure transferring again above zero is the cleanest invalidation set off that spot accumulation confirms the futures-led transfer.

The structural hole between 2026 and 2022 additionally offers the bull case a basis. Bitcoin now has regulated US spot ETFs, deeper institutional infrastructure, and a persistent corporate-treasury bid that didn’t exist 4 years in the past.

Even CryptoQuant’s Apr. 1 be aware, which flagged deep contraction in spot demand, acknowledged that ETF and company shopping for had been accelerating.

The bull case runs on these patrons scaling up quick sufficient to drag spot demand again into optimistic territory. If ETF inflows resume over a sustained window and the futures-to-spot quantity ratio narrows towards the broader market’s 3x studying, the market construction argument weakens by itself phrases.

The bear case

The bear case wants solely leveraged merchants to cut back publicity earlier than spot demand turns optimistic. It requires solely that leveraged merchants begin decreasing publicity earlier than spot demand turns optimistic.

At $54 billion in open curiosity, even a partial unwind produces giant absolute promoting quantity, and with spot quantity working at roughly $4 billion a day, the market lacks the depth to soak up a speedy unwind with out a onerous value drop.

The reflexivity compounds the chance, since falling costs push leveraged longs towards liquidation, liquidations press costs decrease, and the cycle feeds itself till spot demand deepens sufficient to carry a ground.

Bear markets finish when demand for spot and futures recovers collectively.

The present setup has futures recovering on their very own, and if that situation holds, Bitcoin has reproduced the demand construction of 2022’s failed rallies. The approaching weeks of on-chain obvious demand and ETF stream tone will decide whether or not April’s bounce joins that listing or separates from it.

Both actual money patrons step in and validate the futures-led transfer, or the market finds out what a leveraged lengthy e book seems like when the spot bid is just too skinny to carry the ground.

{kind=link}