Why Accenture is larger than a discretionary consulting story

Accenture (NYSE: ACN) is commonly handled like a traditional consulting inventory, which suggests traders are likely to give attention to whether or not enterprise shoppers are nervous, whether or not discretionary tasks are slowing, and whether or not bookings are about to melt. That lens captures a part of the story, however not sufficient of it. Accenture’s personal disclosures level to a enterprise that’s broader, extra embedded, and extra operationally sturdy than a plain advisory mannequin.

In its FY2025 annual report, Accenture stated it serves greater than 9,000 shoppers, together with three quarters of the Fortune World 100 and 500, and that it has partnered with 195 of its prime 200 shoppers for 10 years or extra. That isn’t the profile of a agency residing solely from quarter to quarter on non-obligatory technique work. It’s the profile of a deeply embedded enterprise operator whose relationships span consulting, managed companies, and huge transformation applications.

The corporate additionally organizes itself round what it calls reinvention companies, not simply consulting. That issues. Accenture is attempting to be the working companion for digital core buildouts, workflow redesign, AI deployment, industry-specific transformation, and managed companies supply throughout an enormous shopper base. If that framing is true, then the inventory needs to be analyzed much less like a discretionary companies vendor and extra like a platform for enterprise change.

What the newest numbers say about bookings, combine, and shopper entrenchment

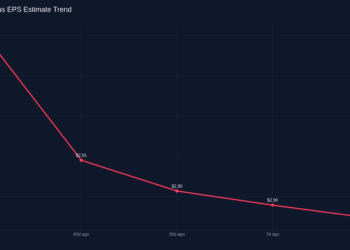

The newest reported quarter helps that interpretation. In fiscal Q2 2026, Accenture reported income of $18.044 billion, up 8% in U.S. {dollars} and 4% in native forex from a yr earlier. New bookings have been $22.1 billion, up 6% in {dollars} and 1% in native forex, whereas diluted EPS rose to $2.93 from $2.82. Working margin improved to 13.8% from 13.5%, in line with the Q2 FY2026 earnings launch and 10-Q.

The combo is very necessary. Within the quarter, consulting income was $8.860 billion and managed companies income was $9.184 billion. That near-even cut up issues as a result of it reveals Accenture just isn’t dependent solely on episodic recommendation work. Managed companies provides the corporate a extra recurring, operationally embedded income stream, whereas consulting feeds future transformation mandates and deeper shopper relationships.

Breadth additionally issues. In Q2 FY2026, Accenture generated $8.9 billion of income within the Americas, $6.6 billion in EMEA, and $2.6 billion in Asia Pacific. Business publicity was additionally unfold throughout Communications, Media & Know-how at $3.1 billion, Monetary Companies at $3.4 billion, Well being & Public Service at $3.7 billion, Merchandise at $5.5 billion, and Sources at $2.4 billion. That diversification lowers dependence on anyone vertical spending cycle.

Administration additionally stated the discretionary atmosphere was unchanged, however shoppers continued to prioritize large-scale transformations, together with turning into AI-ready. That may be a essential distinction. It suggests weaker urge for food in softer challenge classes can coexist with sturdy spending on giant, strategic workflow change, which is the place Accenture needs to take a seat.

Why expertise scale and managed companies matter extra within the AI period

Accenture’s greatest moat could also be its capacity to transform shopper belief and labor scale into execution capability. The FY2025 annual report stated the corporate employed about 779,000 folks at year-end, whereas the Q2 FY2026 truth sheet put the depend at 786,000. That workforce scale issues as a result of giant enterprises don’t simply want concepts; they want techniques built-in, processes redesigned, compliance dealt with, and transformation work delivered throughout geographies.

The corporate’s FY2025 numbers reinforce that this scale is tied to money technology, not simply headcount. Income for FY2025 was $69.7 billion, new bookings have been $80.6 billion, book-to-bill was 1.2, and free money movement was $10.9 billion, in line with the annual report. Money returned to shareholders was $8.3 billion, together with $4.6 billion of repurchases and $3.7 billion of dividends. These are robust numbers for an organization that’s nonetheless investing closely in functionality buildout.

AI is the place the mannequin is being examined subsequent. Accenture highlighted a $3 billion multi-year funding in generative AI and stated FY2025 included a file 129 quarterly shopper bookings of greater than $100 million. The purpose just isn’t that AI routinely ensures progress. It’s that Accenture is attempting to place AI as one other layer of enterprise entrenchment. If shoppers use Accenture not simply to advise on AI, however to revamp workflows, migrate knowledge, function techniques, and handle ongoing processes, then AI can deepen the managed-services and reinvention thesis somewhat than merely create a burst of consulting income.

That’s the reason expertise scale issues greater than ever. In an AI transition, shoppers usually are not simply shopping for software program licenses or slide decks. They’re shopping for implementation capability, area experience, and the flexibility to coordinate giant change applications with out breaking core operations.

What traders ought to watch subsequent: bookings high quality, margin self-discipline, and AI conversion

The principle threat is that traders overestimate how rapidly AI enthusiasm turns into sturdy income. Accenture nonetheless operates in an atmosphere the place administration says discretionary spending is unchanged, which is a well mannered method of claiming components of the market stay cautious. If AI work stays slender, experimental, or principally advisory, then the platform thesis is weaker than it seems.

Bookings high quality is the following factor to look at. A big bookings quantity issues much less whether it is concentrated in lower-margin or shorter-duration work. The stronger sign is whether or not bookings maintain supporting each consulting and managed companies progress throughout sectors and geographies. Margin self-discipline issues too, as a result of an organization with almost 800,000 workers can lose working leverage if utilization slips or hiring outruns demand.

Nonetheless, the broader conclusion is evident. Accenture shouldn’t be understood primarily as a cyclical advisor ready for macro confidence to enhance. It’s higher understood as a reinvention platform with lengthy shopper tenures, significant managed-services depth, broad world attain, and sufficient expertise scale to stay related as enterprise workflows transfer towards AI-heavy transformation.

Key Indicators for Buyers

- The consulting-versus-managed-services combine ought to stay central, as a result of a wholesome managed-services base makes the enterprise extra sturdy than a pure advisory mannequin.

- Bookings high quality issues greater than headline bookings quantity if traders need to choose whether or not transformation demand is actually staying resilient.

- AI conversion needs to be watched by means of precise income, long-duration contracts, and workflow entrenchment somewhat than by means of narrative alone.

- Margin self-discipline issues as a result of Accenture’s scale is a bonus provided that utilization and supply economics stay wholesome.

- Consumer tenure and cross-industry breadth stay strategic belongings, since they assist Accenture maintain monetizing giant enterprise transformations even when discretionary work is gentle.

Sources

- https://newsroom.accenture.com/information/2026/accenture-reports-second-quarter-fiscal-2026-results

- https://newsroom.accenture.com/fact-sheet

- https://www.accenture.com/content material/dam/accenture/closing/accenture-com/document-4/Annual-Report-2025.pdf

- https://www.sec.gov/Archives/edgar/knowledge/1467373/000146737325000217/acn-20250831.htm

Why Accenture is larger than a discretionary consulting story

Accenture (NYSE: ACN) is commonly handled like a traditional consulting inventory, which suggests traders are likely to give attention to whether or not enterprise shoppers are nervous, whether or not discretionary tasks are slowing, and whether or not bookings are about to melt. That lens captures a part of the story, however not sufficient of it. Accenture’s personal disclosures level to a enterprise that’s broader, extra embedded, and extra operationally sturdy than a plain advisory mannequin.

In its FY2025 annual report, Accenture stated it serves greater than 9,000 shoppers, together with three quarters of the Fortune World 100 and 500, and that it has partnered with 195 of its prime 200 shoppers for 10 years or extra. That isn’t the profile of a agency residing solely from quarter to quarter on non-obligatory technique work. It’s the profile of a deeply embedded enterprise operator whose relationships span consulting, managed companies, and huge transformation applications.

The corporate additionally organizes itself round what it calls reinvention companies, not simply consulting. That issues. Accenture is attempting to be the working companion for digital core buildouts, workflow redesign, AI deployment, industry-specific transformation, and managed companies supply throughout an enormous shopper base. If that framing is true, then the inventory needs to be analyzed much less like a discretionary companies vendor and extra like a platform for enterprise change.

What the newest numbers say about bookings, combine, and shopper entrenchment

The newest reported quarter helps that interpretation. In fiscal Q2 2026, Accenture reported income of $18.044 billion, up 8% in U.S. {dollars} and 4% in native forex from a yr earlier. New bookings have been $22.1 billion, up 6% in {dollars} and 1% in native forex, whereas diluted EPS rose to $2.93 from $2.82. Working margin improved to 13.8% from 13.5%, in line with the Q2 FY2026 earnings launch and 10-Q.

The combo is very necessary. Within the quarter, consulting income was $8.860 billion and managed companies income was $9.184 billion. That near-even cut up issues as a result of it reveals Accenture just isn’t dependent solely on episodic recommendation work. Managed companies provides the corporate a extra recurring, operationally embedded income stream, whereas consulting feeds future transformation mandates and deeper shopper relationships.

Breadth additionally issues. In Q2 FY2026, Accenture generated $8.9 billion of income within the Americas, $6.6 billion in EMEA, and $2.6 billion in Asia Pacific. Business publicity was additionally unfold throughout Communications, Media & Know-how at $3.1 billion, Monetary Companies at $3.4 billion, Well being & Public Service at $3.7 billion, Merchandise at $5.5 billion, and Sources at $2.4 billion. That diversification lowers dependence on anyone vertical spending cycle.

Administration additionally stated the discretionary atmosphere was unchanged, however shoppers continued to prioritize large-scale transformations, together with turning into AI-ready. That may be a essential distinction. It suggests weaker urge for food in softer challenge classes can coexist with sturdy spending on giant, strategic workflow change, which is the place Accenture needs to take a seat.

Why expertise scale and managed companies matter extra within the AI period

Accenture’s greatest moat could also be its capacity to transform shopper belief and labor scale into execution capability. The FY2025 annual report stated the corporate employed about 779,000 folks at year-end, whereas the Q2 FY2026 truth sheet put the depend at 786,000. That workforce scale issues as a result of giant enterprises don’t simply want concepts; they want techniques built-in, processes redesigned, compliance dealt with, and transformation work delivered throughout geographies.

The corporate’s FY2025 numbers reinforce that this scale is tied to money technology, not simply headcount. Income for FY2025 was $69.7 billion, new bookings have been $80.6 billion, book-to-bill was 1.2, and free money movement was $10.9 billion, in line with the annual report. Money returned to shareholders was $8.3 billion, together with $4.6 billion of repurchases and $3.7 billion of dividends. These are robust numbers for an organization that’s nonetheless investing closely in functionality buildout.

AI is the place the mannequin is being examined subsequent. Accenture highlighted a $3 billion multi-year funding in generative AI and stated FY2025 included a file 129 quarterly shopper bookings of greater than $100 million. The purpose just isn’t that AI routinely ensures progress. It’s that Accenture is attempting to place AI as one other layer of enterprise entrenchment. If shoppers use Accenture not simply to advise on AI, however to revamp workflows, migrate knowledge, function techniques, and handle ongoing processes, then AI can deepen the managed-services and reinvention thesis somewhat than merely create a burst of consulting income.

That’s the reason expertise scale issues greater than ever. In an AI transition, shoppers usually are not simply shopping for software program licenses or slide decks. They’re shopping for implementation capability, area experience, and the flexibility to coordinate giant change applications with out breaking core operations.

What traders ought to watch subsequent: bookings high quality, margin self-discipline, and AI conversion

The principle threat is that traders overestimate how rapidly AI enthusiasm turns into sturdy income. Accenture nonetheless operates in an atmosphere the place administration says discretionary spending is unchanged, which is a well mannered method of claiming components of the market stay cautious. If AI work stays slender, experimental, or principally advisory, then the platform thesis is weaker than it seems.

Bookings high quality is the following factor to look at. A big bookings quantity issues much less whether it is concentrated in lower-margin or shorter-duration work. The stronger sign is whether or not bookings maintain supporting each consulting and managed companies progress throughout sectors and geographies. Margin self-discipline issues too, as a result of an organization with almost 800,000 workers can lose working leverage if utilization slips or hiring outruns demand.

Nonetheless, the broader conclusion is evident. Accenture shouldn’t be understood primarily as a cyclical advisor ready for macro confidence to enhance. It’s higher understood as a reinvention platform with lengthy shopper tenures, significant managed-services depth, broad world attain, and sufficient expertise scale to stay related as enterprise workflows transfer towards AI-heavy transformation.

Key Indicators for Buyers

- The consulting-versus-managed-services combine ought to stay central, as a result of a wholesome managed-services base makes the enterprise extra sturdy than a pure advisory mannequin.

- Bookings high quality issues greater than headline bookings quantity if traders need to choose whether or not transformation demand is actually staying resilient.

- AI conversion needs to be watched by means of precise income, long-duration contracts, and workflow entrenchment somewhat than by means of narrative alone.

- Margin self-discipline issues as a result of Accenture’s scale is a bonus provided that utilization and supply economics stay wholesome.

- Consumer tenure and cross-industry breadth stay strategic belongings, since they assist Accenture maintain monetizing giant enterprise transformations even when discretionary work is gentle.

Sources

- https://newsroom.accenture.com/information/2026/accenture-reports-second-quarter-fiscal-2026-results

- https://newsroom.accenture.com/fact-sheet

- https://www.accenture.com/content material/dam/accenture/closing/accenture-com/document-4/Annual-Report-2025.pdf

- https://www.sec.gov/Archives/edgar/knowledge/1467373/000146737325000217/acn-20250831.htm

{kind=link}