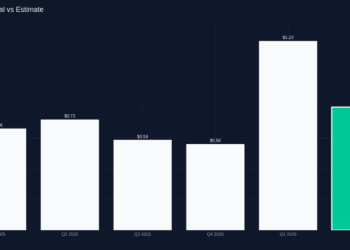

Lloyds Banking Group plc (NYSE: LYG) nonetheless attracts consideration as a U.Ok. dividend financial institution, however its newest quarter makes a stronger case that the inventory needs to be judged on earnings resilience, capital era, and credit score efficiency. Within the first quarter of 2026, Lloyds reported statutory revenue earlier than tax of £2.0 billion versus £1.5 billion a yr earlier, web earnings of £4.8 billion, up 9%, web curiosity earnings of £3.6 billion, up 8%, and a banking web curiosity margin of three.17%, up 14 foundation factors yr over yr. Return on tangible fairness was 17.0%, in contrast with 12.6% a yr earlier, and administration mentioned it nonetheless expects return on tangible fairness for full-year 2026 to be higher than 16%.

These figures matter greater than the dividend label as a result of they present a financial institution nonetheless benefiting from hedge earnings, lending development, and steady credit score. The true query for traders is whether or not Lloyds can maintain translating these benefits into earnings and capital returns as U.Ok. charges and credit score circumstances evolve.

Why Lloyds needs to be judged on margin resilience, capital returns, and credit score high quality somewhat than on a dividend label alone

The primary purpose is that Lloyds remains to be proving it may well develop core earnings even whereas asset margin stress persists. The group mentioned underlying web curiosity earnings within the first quarter was £3.569 billion, up 1% from the fourth quarter of 2025, as a rising structural hedge contribution offset headwinds from asset margin compression. Common interest-earning banking belongings rose to £473.5 billion from £470.3 billion within the prior quarter, reflecting development throughout the Retail division, led by U.Ok. mortgages, and development in Business Banking.

Which means Lloyds will not be merely coasting on a static deposit base or legacy price tailwind. The structural hedge stays a serious earnings engine. As of March 31, 2026, the notional stability of the sterling structural hedge was £246 billion, up from £244 billion at year-end 2025, and the group generated £1.6 billion of complete earnings from structural hedge balances within the first three months of 2026 versus £1.2 billion a yr earlier. Administration now expects structural hedge earnings to be higher than £7.0 billion in 2026 and higher than £8.0 billion in 2027.

The balance-sheet developments assist that story. Lending reached £486.2 billion, up £5.1 billion within the quarter and up 4% yr over yr, with development throughout all enterprise strains. Buyer deposits have been £495.9 billion, down solely £0.6 billion within the quarter and nonetheless up 2% yr over yr, as a £3.1 billion discount in Retail deposits was partly offset by £2.3 billion development in Business Banking deposits. These are the sorts of developments that matter greater than a dividend headline as a result of they assist decide whether or not Lloyds can maintain compounding web curiosity earnings with out stretching threat.

Capital return is a part of the case, however it’s downstream from working power. Tangible web belongings per share rose to 57.9 pence from 57.0 pence at December 31, 2025, even after the continued share buyback introduced in January. By March 31, the group had repurchased about 0.6 billion shares at a price of £0.7 billion and a mean value of 97.7 pence. That’s helpful, however it solely works as a result of the earnings and capital engine stays intact.

What the newest reported web curiosity earnings, capital ratios, impairments, and U.Ok. loan-growth context say about upside and threat now

The very best signal within the quarter is that Lloyds paired greater earnings with disciplined credit score. Underlying impairment was £295 million versus £309 million a yr earlier, producing an asset high quality ratio of 25 foundation factors. The group mentioned the cost stayed low due to robust and steady credit score efficiency throughout portfolios and advantages from quarterly mannequin calibrations. It additionally mentioned noticed Business Banking fees have been very low within the quarter, and it continues to anticipate the asset high quality ratio to be about 25 foundation factors for 2026.

That doesn’t imply threat has disappeared. The quarter included a £101 million cost from up to date a number of financial eventualities, reflecting a £151 million affect from a deterioration within the financial outlook tied to the Center East battle, partly offset by a £50 million launch of a post-model adjustment for tariff and political disruption dangers. So Lloyds nonetheless has to navigate a macro backdrop that may change shortly, even when present credit score efficiency seems to be calm.

Capital stays strong sufficient to assist that navigation. Lloyds reported robust capital era of 41 foundation factors within the quarter and a CET1 ratio of 13.4% after the bizarre dividend accrual. Danger-weighted belongings have been £240.8 billion, up from £235.5 billion at year-end 2025, reflecting lending-driven development. The group additionally reported a complete capital ratio of 18.2%, a loan-to-deposit ratio of 98%, a liquidity protection ratio of 144%, and a web steady funding ratio of 123%. These are wholesome figures, however in addition they present the financial institution is utilizing stability sheet capability somewhat than sitting on it.

The price line is one other factor to look at. Lloyds mentioned the associated fee:earnings ratio was 51.9% versus 58.1% a yr earlier and reiterated that it expects the 2026 value:earnings ratio to be beneath 50%, with working prices nonetheless anticipated to be lower than £9.9 billion. If administration delivers that whereas conserving the asset high quality ratio close to 25 foundation factors and web curiosity earnings above £14.9 billion for the yr, the case for Lloyds seems to be a lot stronger than a easy dividend display screen.

Key Alerts for Traders

- Lloyds’ earnings case nonetheless begins with margin resilience, with web curiosity earnings of £3.6 billion and a banking web curiosity margin of three.17% exhibiting the hedge remains to be doing heavy lifting.

- Lending development to £486.2 billion alongside broadly steady deposits at £495.9 billion suggests the financial institution remains to be rising the stability sheet with out apparent funding stress.

- A 13.4% CET1 ratio after the dividend accrual and 41 foundation factors of quarterly capital era maintain capital returns credible, however rising risk-weighted belongings imply self-discipline nonetheless issues.

- The 25 foundation level asset high quality ratio stays benign, but the quarter’s £101 million MES cost is a reminder that Lloyds will not be insulated from macro shocks.

- If Lloyds can maintain web curiosity earnings above £14.9 billion in 2026 whereas taking the associated fee:earnings ratio beneath 50%, the inventory will look extra like an earnings-compounder than a easy high-yield financial institution.

Sources

- https://www.lloydsbankinggroup.com/belongings/pdfs/traders/financial-performance/lloyds-banking-group-plc/2026/q1/2026-lbg-q1-ims.pdf

- https://www.lloydsbankinggroup.com/belongings/pdfs/traders/financial-performance/lloyds-banking-group-plc/2026/q1/2026-lbg-q1-shareholder-faqs.pdf

- https://www.lloydsbankinggroup.com/traders.html

{kind=link}