Picture supply: Getty Pictures

In case you’re a type of traders who took an opportunity on Rolls-Royce (LSE:RR) shares once they traded for round 60p, this yr you’d obtain round 13% of your authentic funding as dividends. That’s an exceptional bonus to enhance the 1,100% share worth appreciation since then.

Reintroduction of dividends

After a five-year hiatus, Rolls-Royce is reinstating dividends. This marks a big milestone in its turnaround. The corporate introduced a 6p per share payout, amounting to £500m, to be distributed in June 2025. This determination follows a stellar 2024 efficiency, with working earnings surging 55% to £2.5bn and free money circulation practically doubling to £2.4bn.

Moreover, Rolls-Royce has launched a £1bn share buyback programme, returning a complete of £1.5bn to shareholders. CEO Tufan Erginbilgic emphasised the agency’s transformation right into a high-performing, resilient enterprise, pushed by robust outcomes throughout all core divisions.

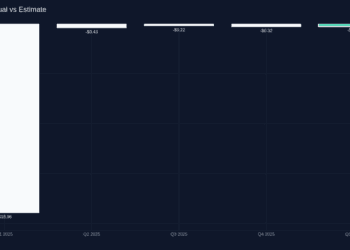

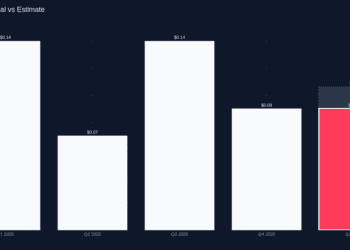

Trying ahead, Rolls-Royce’s dividend outlook is promising, with analysts forecasting regular development. The payout is predicted to rise from 6p in 2025 to 7.8p in 2026 and 9.01p in 2027, reflecting annual will increase of 30% and 16%, respectively. The corporate goals to distribute 30%-40% of underlying pre-tax earnings as dividends, supported by sturdy earnings development.

Pre-tax revenue is projected to succeed in £2.86bn in 2025 and £3.18bn by 2027. Nevertheless, the dividend yield stays modest at underneath 1% on the present worth, reflecting the inventory’s latest rally. Regardless of this, Rolls-Royce’s enhancing money circulation and profitability underpin its long-term dividend potential.

Driving the volatility

President Trump’s tariffs will doubtlessly create appreciable challenges for Rolls-Royce. As a significant exporter of plane engines and energy techniques, the corporate depends closely on world provide chains and worldwide commerce.

The tariffs, together with a levy on British exports to the US are driving up manufacturing prices and disrupting operations. In concept, the tariffs would make a UK firm much less aggressive within the US market.

Nevertheless, it’s vital to notice that whereas 31% of the corporate’s gross sales are within the US, 30% of its manufacturing capability is within the States too. This could mitigate a few of the affect.

The underside line

I’m going to begin by saying that I wouldn’t purchase Rolls-Royce inventory right this moment for the dividends within the close to time period. Nevertheless, I’d spotlight that it is a enterprise that’s booming, and reasonable dividend will increase over time can actually add up. Simply have a look at the instance of Warren Buffett and Coca-Cola — he now receives round a 60% yield based mostly on the worth of his first investments. That’s one thing to consider.

Extra typically, Rolls-Royce has benefitted from robust demand for long-haul journey and defence contracts, with projected working margins of 13%-15% by 2027. Rolls-Royce’s strategic concentrate on money circulation era and cost-cutting positions has additionally made it extra resilient.

Nevertheless, dangers at the moment are elevated. Trump’s tariffs threaten provide chain stability, might inflate manufacturing prices and injury air journey demand. Proper now, I’m simply watching the volatility from a distance. I don’t anticipate so as to add to my holdings instantly even at this barely extra enticing 25 instances earnings.

Picture supply: Getty Pictures

In case you’re a type of traders who took an opportunity on Rolls-Royce (LSE:RR) shares once they traded for round 60p, this yr you’d obtain round 13% of your authentic funding as dividends. That’s an exceptional bonus to enhance the 1,100% share worth appreciation since then.

Reintroduction of dividends

After a five-year hiatus, Rolls-Royce is reinstating dividends. This marks a big milestone in its turnaround. The corporate introduced a 6p per share payout, amounting to £500m, to be distributed in June 2025. This determination follows a stellar 2024 efficiency, with working earnings surging 55% to £2.5bn and free money circulation practically doubling to £2.4bn.

Moreover, Rolls-Royce has launched a £1bn share buyback programme, returning a complete of £1.5bn to shareholders. CEO Tufan Erginbilgic emphasised the agency’s transformation right into a high-performing, resilient enterprise, pushed by robust outcomes throughout all core divisions.

Trying ahead, Rolls-Royce’s dividend outlook is promising, with analysts forecasting regular development. The payout is predicted to rise from 6p in 2025 to 7.8p in 2026 and 9.01p in 2027, reflecting annual will increase of 30% and 16%, respectively. The corporate goals to distribute 30%-40% of underlying pre-tax earnings as dividends, supported by sturdy earnings development.

Pre-tax revenue is projected to succeed in £2.86bn in 2025 and £3.18bn by 2027. Nevertheless, the dividend yield stays modest at underneath 1% on the present worth, reflecting the inventory’s latest rally. Regardless of this, Rolls-Royce’s enhancing money circulation and profitability underpin its long-term dividend potential.

Driving the volatility

President Trump’s tariffs will doubtlessly create appreciable challenges for Rolls-Royce. As a significant exporter of plane engines and energy techniques, the corporate depends closely on world provide chains and worldwide commerce.

The tariffs, together with a levy on British exports to the US are driving up manufacturing prices and disrupting operations. In concept, the tariffs would make a UK firm much less aggressive within the US market.

Nevertheless, it’s vital to notice that whereas 31% of the corporate’s gross sales are within the US, 30% of its manufacturing capability is within the States too. This could mitigate a few of the affect.

The underside line

I’m going to begin by saying that I wouldn’t purchase Rolls-Royce inventory right this moment for the dividends within the close to time period. Nevertheless, I’d spotlight that it is a enterprise that’s booming, and reasonable dividend will increase over time can actually add up. Simply have a look at the instance of Warren Buffett and Coca-Cola — he now receives round a 60% yield based mostly on the worth of his first investments. That’s one thing to consider.

Extra typically, Rolls-Royce has benefitted from robust demand for long-haul journey and defence contracts, with projected working margins of 13%-15% by 2027. Rolls-Royce’s strategic concentrate on money circulation era and cost-cutting positions has additionally made it extra resilient.

Nevertheless, dangers at the moment are elevated. Trump’s tariffs threaten provide chain stability, might inflate manufacturing prices and injury air journey demand. Proper now, I’m simply watching the volatility from a distance. I don’t anticipate so as to add to my holdings instantly even at this barely extra enticing 25 instances earnings.

{kind=link}