AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Inventory $12.94 (+2.0%)

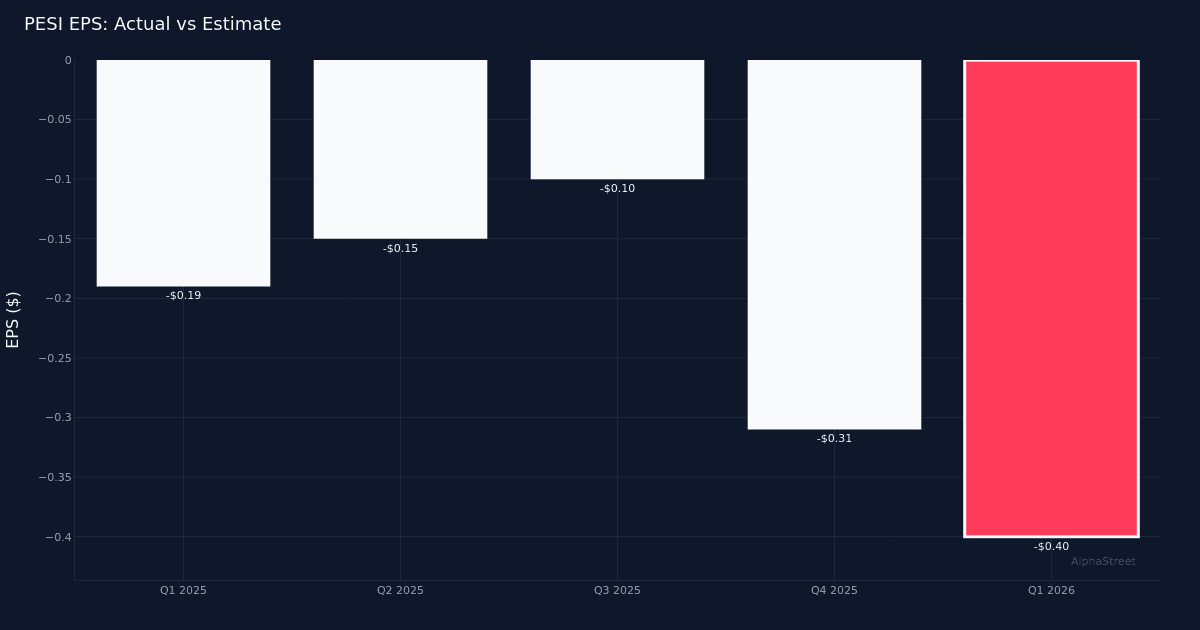

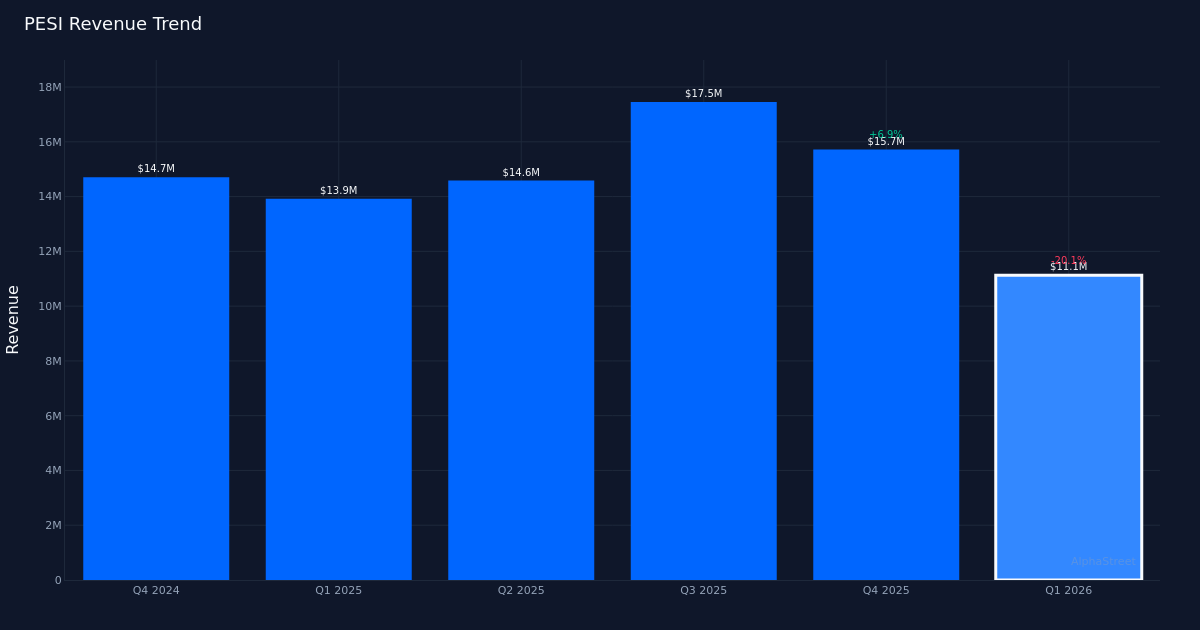

Wider Miss. Perma-Repair Environmental Companies, Inc. (NASDAQ: PESI) reported disappointing Q1 2026 outcomes, posting a internet loss per share of $0.40 in comparison with the anticipated lack of $0.24, representing a 66.7% miss in comparison with Wall Road projections. Income totaled $11.1M for the quarter, declining 20.1% from $13.9M within the year-ago interval. The corporate’s internet loss widened to $7.5M, with the per-share loss increasing 110.5% from the $0.19 loss reported in Q1 2025. The inventory traded up 2.0% to $12.94 following the discharge, suggesting buyers might have already anticipated weaker outcomes or are trying previous near-term challenges within the nuclear and dangerous waste administration house.

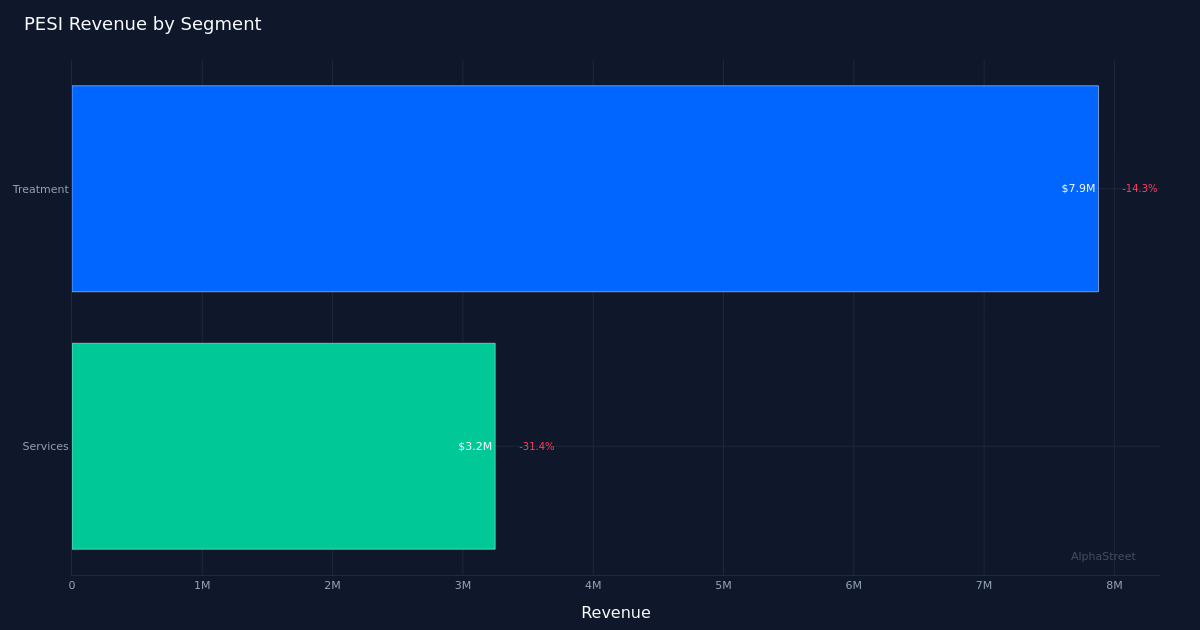

Remedy Section Pressures. The Remedy section, which led income technology at $7.9M, skilled a 14.3% year-over-year decline as the corporate navigated softer demand situations in its core waste processing operations. This weak spot within the flagship Remedy enterprise drove the vast majority of the consolidated income decline, elevating questions on contract timing and quantity developments within the nuclear providers sector. The absence of disclosed efficiency metrics from different enterprise segments leaves buyers with restricted visibility into potential offsetting strengths or further strain factors throughout the portfolio.

Margin Deterioration. The disproportionate widening of the online loss relative to the income decline alerts vital margin compression in the course of the quarter. Whereas income fell 20.1%, the per-share loss greater than doubled on a year-over-year foundation, indicating the corporate confronted operational deleveraging as mounted prices weighed closely in opposition to the decrease income base. This means structural value challenges slightly than non permanent quantity fluctuations, a much less favorable dynamic that raises considerations concerning the sustainability of the present value construction given the corporate’s scale of operations.

Wall Road Maintains Help. Regardless of the disappointing quarterly efficiency, analyst sentiment stays constructive with Wall Road consensus standing at 4 purchase rankings and 1 maintain score, with no promote suggestions. This vote of confidence suggests the funding group views the present weak spot as cyclical slightly than structural, probably reflecting expectations for a restoration in contract exercise or useful regulatory developments within the nuclear waste administration trade. The absence of up to date steerage within the launch, nevertheless, leaves uncertainty round administration’s visibility right into a turnaround timeline.

What to Watch: The trail to profitability hinges on administration’s capacity to stabilize Remedy section volumes whereas right-sizing the fee construction for present income ranges. Buyers ought to give attention to contract pipeline commentary, potential margin enchancment initiatives, and any indicators of demand restoration within the nuclear waste processing market when steerage turns into accessible.

This content material is for informational functions solely and shouldn’t be thought of funding recommendation. AlphaStreet Intelligence analyzes monetary information utilizing AI to ship quick and correct market info. Human editors confirm content material.

AlphaStreet Newsdesk powered by AlphaStreet Intelligence

Inventory $12.94 (+2.0%)

Wider Miss. Perma-Repair Environmental Companies, Inc. (NASDAQ: PESI) reported disappointing Q1 2026 outcomes, posting a internet loss per share of $0.40 in comparison with the anticipated lack of $0.24, representing a 66.7% miss in comparison with Wall Road projections. Income totaled $11.1M for the quarter, declining 20.1% from $13.9M within the year-ago interval. The corporate’s internet loss widened to $7.5M, with the per-share loss increasing 110.5% from the $0.19 loss reported in Q1 2025. The inventory traded up 2.0% to $12.94 following the discharge, suggesting buyers might have already anticipated weaker outcomes or are trying previous near-term challenges within the nuclear and dangerous waste administration house.

Remedy Section Pressures. The Remedy section, which led income technology at $7.9M, skilled a 14.3% year-over-year decline as the corporate navigated softer demand situations in its core waste processing operations. This weak spot within the flagship Remedy enterprise drove the vast majority of the consolidated income decline, elevating questions on contract timing and quantity developments within the nuclear providers sector. The absence of disclosed efficiency metrics from different enterprise segments leaves buyers with restricted visibility into potential offsetting strengths or further strain factors throughout the portfolio.

Margin Deterioration. The disproportionate widening of the online loss relative to the income decline alerts vital margin compression in the course of the quarter. Whereas income fell 20.1%, the per-share loss greater than doubled on a year-over-year foundation, indicating the corporate confronted operational deleveraging as mounted prices weighed closely in opposition to the decrease income base. This means structural value challenges slightly than non permanent quantity fluctuations, a much less favorable dynamic that raises considerations concerning the sustainability of the present value construction given the corporate’s scale of operations.

Wall Road Maintains Help. Regardless of the disappointing quarterly efficiency, analyst sentiment stays constructive with Wall Road consensus standing at 4 purchase rankings and 1 maintain score, with no promote suggestions. This vote of confidence suggests the funding group views the present weak spot as cyclical slightly than structural, probably reflecting expectations for a restoration in contract exercise or useful regulatory developments within the nuclear waste administration trade. The absence of up to date steerage within the launch, nevertheless, leaves uncertainty round administration’s visibility right into a turnaround timeline.

What to Watch: The trail to profitability hinges on administration’s capacity to stabilize Remedy section volumes whereas right-sizing the fee construction for present income ranges. Buyers ought to give attention to contract pipeline commentary, potential margin enchancment initiatives, and any indicators of demand restoration within the nuclear waste processing market when steerage turns into accessible.

This content material is for informational functions solely and shouldn’t be thought of funding recommendation. AlphaStreet Intelligence analyzes monetary information utilizing AI to ship quick and correct market info. Human editors confirm content material.

{kind=link}