Why O’Reilly is greater than an auto-parts retailer

O’Reilly Automotive (ORLY) is usually framed as a simple beneficiary of an growing older automobile fleet and regular restore demand. That rationalization isn’t mistaken, however it’s incomplete. The corporate’s edge is much less about generic publicity to automobile upkeep and extra about execution inside an advanced success community. O’Reilly serves each do-it-yourself prospects {and professional} restore retailers, and its potential to get the best half to the best place shortly is what turns a mature retail class right into a sturdy compounding story.

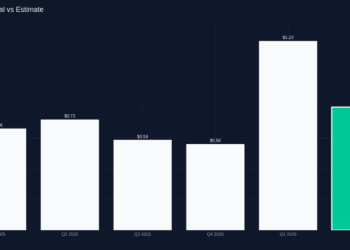

The primary quarter of 2026 confirmed why that distinction issues. Gross sales elevated $424 million, or 10%, to $4.56 billion. Comparable retailer gross sales elevated 8.1%, gross revenue rose 11% to $2.35 billion, working earnings elevated 14% to $842 million, and diluted earnings per share rose 16% to $0.72. These are robust outcomes for an organization in a class that’s typically handled as gradual and purely cyclical.

How the dual-market technique and distribution density assist returns

O’Reilly describes its mannequin as a dual-market technique serving each do-it-yourself prospects {and professional} service suppliers. That issues as a result of the skilled aspect relies upon closely on uptime, supply velocity, and breadth of stock. A store that wants a hard-to-find half the identical day isn’t making the choice on value alone.

That is the place O’Reilly’s community turns into the moat. At December 31, 2025, the corporate operated 6,447 shops in the US and Puerto Rico, 112 shops in Mexico, and 26 shops in Canada. It additionally operated 32 distribution facilities and 399 hub shops. In response to the annual report, the distribution community provides shops same-day or in a single day entry to greater than 156,000 stock-keeping items, whereas hub shops present same-day entry to a median of 63,000 SKUs, with enhanced hubs carrying as much as about 115,000 SKUs. Greater than 95% of shops obtain a number of same-day deliveries and weekend deliveries of hard-to-find components from distribution facilities and hub shops.

These particulars clarify why administration highlighted first-quarter 2026 double-digit skilled development and mid-single-digit DIY development in its earnings launch commentary. The community is constructed to win the skilled channel, the place reliability and repair ranges can matter greater than a marginal value distinction. That doesn’t make shopper demand irrelevant, but it surely does imply O’Reilly has a extra defensible working mannequin than a easy retailer promoting commodity components off the shelf.

Why money era and repurchases nonetheless matter

The mannequin additionally produces actual money. Within the first quarter of 2026, web money supplied by working actions elevated to $1.033 billion from $755 million a 12 months earlier. O’Reilly ended March 31, 2026, with $252.6 million of money and money equivalents, $5.810 billion of stock, and $6.195 billion of long-term debt. That stability sheet isn’t conservative in a standard sense, but it surely displays an organization comfy utilizing leverage alongside very constant working efficiency.

Capital allocation stays a significant a part of the thesis. Through the first quarter of 2026, O’Reilly repurchased 10.0 million shares for $923 million at a median value of $92.45, and it purchased one other 3.6 million shares for $338 million after quarter-end via the date of the discharge. Buybacks alone don’t create a moat, however in a enterprise that retains posting robust comparable gross sales and excessive incremental margins, they’ll materially amplify per-share development.

The working mannequin’s high quality reveals up in profitability too. Gross margin improved to 51.5% of gross sales within the first quarter of 2026 from 51.3% a 12 months earlier, whereas working margin expanded to 18.5% from 17.9%. These are unusually robust retail economics they usually reinforce the concept O’Reilly is promoting availability, velocity, and repair, not simply auto components.

What traders ought to watch subsequent throughout comparable gross sales, stock, and professional demand

The most important query is whether or not O’Reilly can maintain translating community density into sustained market-share positive aspects within the skilled channel. Administration’s commentary suggests the reply continues to be sure, however that should maintain even when shopper spending will get choppier. The primary quarter was helped by each skilled and DIY demand, but the extra sturdy edge possible stays the skilled aspect as a result of service ranges and stock availability create switching prices.

Buyers must also watch stock productiveness and margin self-discipline. Carrying a deep assortment is a power provided that the corporate can maintain turns wholesome and success quick. If O’Reilly maintains robust comparable gross sales, protects margins, and retains changing earnings into money, the inventory will maintain wanting much less like a generic retailer and extra like a specialised logistics-and-service compounder.

Key Alerts for Buyers

- First-quarter 2026 gross sales elevated 10% to $4.56 billion, and comparable retailer gross sales rose 8.1%.

- Gross margin improved to 51.5% of gross sales, and working margin elevated to 18.5% within the first quarter of 2026.

- O’Reilly operated 6,447 U.S. and Puerto Rico shops, 112 Mexico shops, 26 Canada shops, 32 distribution facilities, and 399 hub shops at year-end 2025.

- Web money supplied by working actions elevated to $1.033 billion within the first quarter of 2026 from $755 million a 12 months earlier.

- The corporate repurchased $923 million of inventory within the first quarter and one other $338 million after quarter-end via the discharge date.

{kind=link}