Most individuals consider a Shares and Shares ISA as a approach to complement their revenue. However what if it might exchange it totally?

In keeping with the most recent figures from the Workplace for Nationwide Statistics, common full-time weekly earnings stand at £766. That works out at roughly £3,064 a month.

Producing that degree of revenue from investments is feasible. The query is how massive an ISA would should be to make it occur.

The revenue goal in context

Changing a month-to-month wage of £3,064 requires annual revenue of £36,768.

Utilizing the extensively adopted 4% withdrawal rule, this suggests an ISA price roughly £919,200.

At first look, that may be a daunting determine.

Nonetheless, it’s price remembering that the earnings benchmarks from the ONS are based mostly on gross revenue, earlier than tax. Against this, a Shares and Shares ISA sits inside a tax-free wrapper, which might scale back the efficient revenue requirement in actual phrases.

Even so, the dimensions of the goal stays vital.

The important thing query isn’t simply what the quantity is, however how lengthy it would realistically take to achieve it.

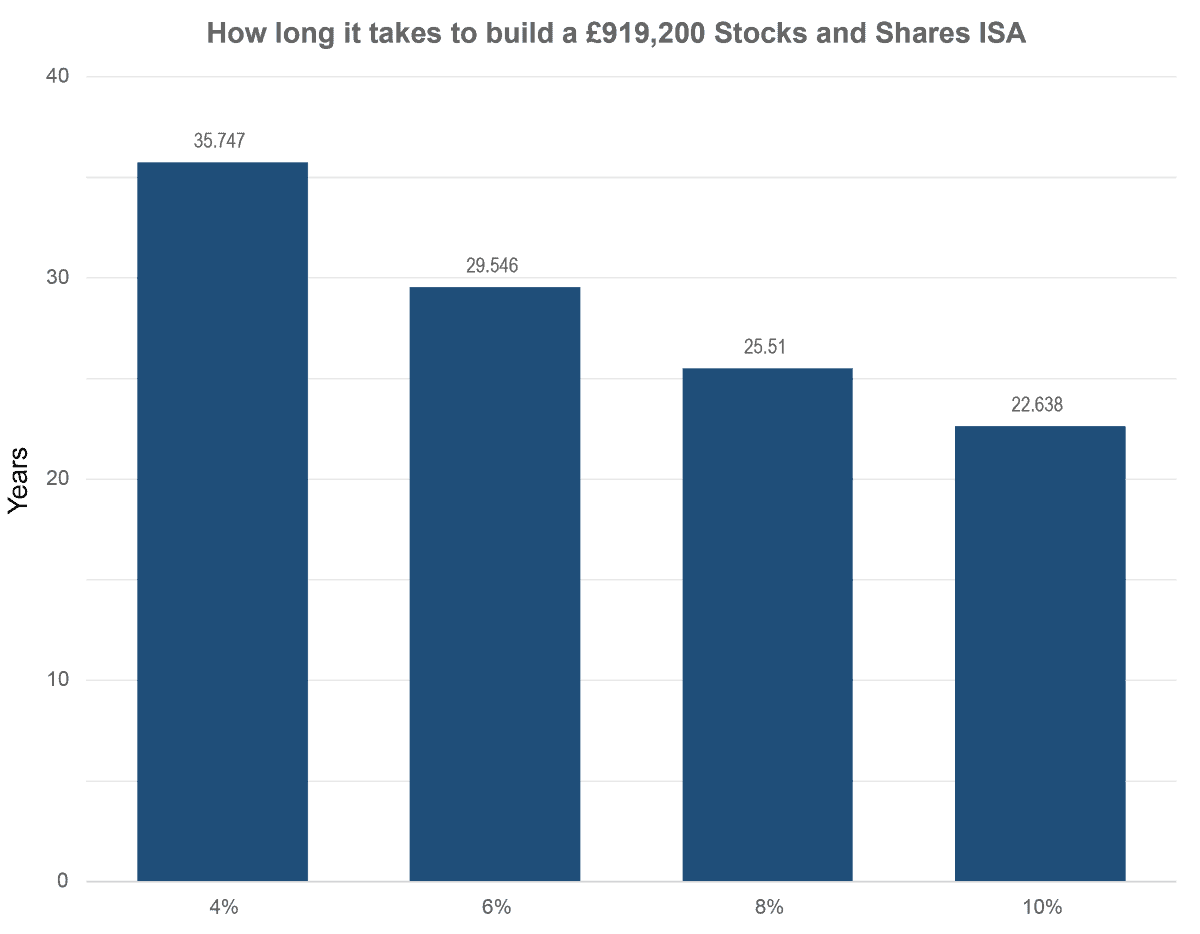

If an investor contributes £12,000 a yr (£1,000 a month), the chart beneath exhibits how lengthy it could take to achieve a £919,200 portfolio below totally different return assumptions.

Chart generated by writer

Please notice that tax remedy relies on the person circumstances of every consumer and could also be topic to alter in future. The content material on this article is supplied for info functions solely. It’s not supposed to be, neither does it represent, any type of tax recommendation. Readers are liable for finishing up their very own due diligence and for acquiring skilled recommendation earlier than making any funding choices.

High quality compounder in observe

That vary of return outcomes highlights why the kind of companies held inside an ISA issues a lot. Shifting from decrease single-digit returns to one thing nearer to eight%-10% a yr is not only a small enchancment — over time, it might dramatically change the top consequence.

One instance of an organization working at a really totally different degree of development high quality is Diploma (LSE: DPLM).

The corporate’s newest half-year outcomes underline that time clearly. Income rose 17% to £851m, supported by 15% natural development — nicely forward of its long-term 10% pattern. This isn’t low-single-digit compounding; it’s double-digit enlargement at scale.

Profitability additionally strengthened meaningfully. Adjusted working revenue elevated 33% to £209m, whereas margins expanded by 300 foundation factors to 24.5%. That mixture of sooner development and rising margins is a trademark of real pricing energy, not simply quantity enlargement.

Earnings momentum was even stronger. Adjusted earnings per share rose 36%, reflecting each operational leverage and disciplined execution throughout the group.

Development drivers

Importantly, this isn’t being pushed by a single lever. Diploma continues to increase by a mixture of natural development and disciplined acquisitions, finishing 15 offers over the previous yr, whereas nonetheless sustaining a conservative stability sheet with leverage at simply 0.8 instances.

The result’s a enterprise delivering development that persistently sits nicely above typical industrial friends — the type of profile that, if sustained, helps the upper return assumptions proven within the ISA chart.

There are dangers, significantly round acquisition execution and sustaining elevated development charges. However the underlying high quality of the compounding engine is evident to me.

Constructing an ISA able to changing a significant degree of revenue is never about one resolution — it’s concerning the constant possession of high-quality compounders over time.

Diploma is one instance of the kind of enterprise that may help that journey, however it isn’t the one one I’m watching intently in the meanwhile.

Do you have to make investments £5,000 in Diploma Plc proper now?

When investing knowledgeable Mark Rogers and his staff have a inventory tip, it might pay to pay attention. In any case, the flagship Twelfth Magpie Share Advisor publication he has run for practically a decade has supplied 1000’s of paying members with prime inventory suggestions from the UK and US markets.

And proper now, Mark thinks there are 6 standout shares that traders ought to think about shopping for. Wish to see if Diploma Plc made the checklist?

Andrew Mackie owns shares in Diploma.

Most individuals consider a Shares and Shares ISA as a approach to complement their revenue. However what if it might exchange it totally?

In keeping with the most recent figures from the Workplace for Nationwide Statistics, common full-time weekly earnings stand at £766. That works out at roughly £3,064 a month.

Producing that degree of revenue from investments is feasible. The query is how massive an ISA would should be to make it occur.

The revenue goal in context

Changing a month-to-month wage of £3,064 requires annual revenue of £36,768.

Utilizing the extensively adopted 4% withdrawal rule, this suggests an ISA price roughly £919,200.

At first look, that may be a daunting determine.

Nonetheless, it’s price remembering that the earnings benchmarks from the ONS are based mostly on gross revenue, earlier than tax. Against this, a Shares and Shares ISA sits inside a tax-free wrapper, which might scale back the efficient revenue requirement in actual phrases.

Even so, the dimensions of the goal stays vital.

The important thing query isn’t simply what the quantity is, however how lengthy it would realistically take to achieve it.

If an investor contributes £12,000 a yr (£1,000 a month), the chart beneath exhibits how lengthy it could take to achieve a £919,200 portfolio below totally different return assumptions.

Chart generated by writer

Please notice that tax remedy relies on the person circumstances of every consumer and could also be topic to alter in future. The content material on this article is supplied for info functions solely. It’s not supposed to be, neither does it represent, any type of tax recommendation. Readers are liable for finishing up their very own due diligence and for acquiring skilled recommendation earlier than making any funding choices.

High quality compounder in observe

That vary of return outcomes highlights why the kind of companies held inside an ISA issues a lot. Shifting from decrease single-digit returns to one thing nearer to eight%-10% a yr is not only a small enchancment — over time, it might dramatically change the top consequence.

One instance of an organization working at a really totally different degree of development high quality is Diploma (LSE: DPLM).

The corporate’s newest half-year outcomes underline that time clearly. Income rose 17% to £851m, supported by 15% natural development — nicely forward of its long-term 10% pattern. This isn’t low-single-digit compounding; it’s double-digit enlargement at scale.

Profitability additionally strengthened meaningfully. Adjusted working revenue elevated 33% to £209m, whereas margins expanded by 300 foundation factors to 24.5%. That mixture of sooner development and rising margins is a trademark of real pricing energy, not simply quantity enlargement.

Earnings momentum was even stronger. Adjusted earnings per share rose 36%, reflecting each operational leverage and disciplined execution throughout the group.

Development drivers

Importantly, this isn’t being pushed by a single lever. Diploma continues to increase by a mixture of natural development and disciplined acquisitions, finishing 15 offers over the previous yr, whereas nonetheless sustaining a conservative stability sheet with leverage at simply 0.8 instances.

The result’s a enterprise delivering development that persistently sits nicely above typical industrial friends — the type of profile that, if sustained, helps the upper return assumptions proven within the ISA chart.

There are dangers, significantly round acquisition execution and sustaining elevated development charges. However the underlying high quality of the compounding engine is evident to me.

Constructing an ISA able to changing a significant degree of revenue is never about one resolution — it’s concerning the constant possession of high-quality compounders over time.

Diploma is one instance of the kind of enterprise that may help that journey, however it isn’t the one one I’m watching intently in the meanwhile.

Do you have to make investments £5,000 in Diploma Plc proper now?

When investing knowledgeable Mark Rogers and his staff have a inventory tip, it might pay to pay attention. In any case, the flagship Twelfth Magpie Share Advisor publication he has run for practically a decade has supplied 1000’s of paying members with prime inventory suggestions from the UK and US markets.

And proper now, Mark thinks there are 6 standout shares that traders ought to think about shopping for. Wish to see if Diploma Plc made the checklist?

Andrew Mackie owns shares in Diploma.

{kind=link}