Picture supply: Getty Photographs

Halma (LSE:HLMA) has been certainly one of my prime FTSE 100 development shares for a while. However the inventory crashed 14% on Thursday (11 June) after the agency launched its full-year earnings.

Is that this my alternative? Or has one thing gone badly improper with one of many UK’s prime long-term compounders of the final 10 years?

What’s occurred?

Halma’s full-year replace reported 16.6% natural income development. And – as I predicted – it’s been 12 months for the photonics division.

This sells tools to information centres, the place demand has clearly been large. Consequently, this a part of the enterprise grew 52%.

Seeing this coming wasn’t particularly arduous work. Diploma – one other FTSE 100 firm – posted largely comparable outcomes not too long ago.

The factor is, buyers cheered Diploma’s announcement prefer it was a hero. However the response to Halma has been fairly totally different.

Apparently, when Diploma sells to information centres, it’s a masterclass. When Halma does it, it’s a cyclical tightrope stroll.

Is that proper? Or is the market’s uneven response an enormous alternative for me to purchase a inventory I’ve had my eye on for some time?

What’s to not like?

Buyers reacted negatively to Halma’s information for 2 causes. The primary is focus.

The agency revealed that its photonics enterprise sells to a single information centre buyer. And that makes up round 20% of its total income.

It additionally accounted for round half of the overall natural development. So development elsewhere within the enterprise was fairly modest.

| Division | Natural Progress |

|---|---|

| Security | 5.9% |

| Environmental & Evaluation | 33.60% |

| Healthcare | 4.90% |

The opposite difficulty is cyclicality. Administration warned that photonics development is more likely to sluggish to 30% subsequent 12 months. That’s nonetheless loads, nevertheless it’s decrease.

Diploma’s report didn’t announce both of those points. The demand difficulty, nonetheless, is more likely to be the identical for each firms.

The focus threat is actual. However buyers shouldn’t overlook the place this obvious downside has come from.

Lengthy-term power

Halma acquired Avo Photonics in 2011 at a modest worth when it was a tiny fraction of its present measurement. And that transfer has labored out spectacularly.

It jogs my memory a little bit of Warren Buffett’s Apple funding. That labored out so properly that it got here to dominate Berkshire Hathaway’s portfolio.

Buyers ought to need Halma to do offers like this so what they need to hope for is extra of the identical.

There are optimistic indicators on this entrance. Within the final 12 months, the agency invested a file £447m and two extra have been accomplished for the reason that finish of the 12 months.

That’s a key long-term power for Halma. It’s an enormous a part of why the inventory has been such funding during the last 10 years.

This isn’t to say buyers ought to ignore the focus threat. However they need to keep in mind why it’s come about.

Is that this my alternative?

Halma is a inventory I’ve had on my radar for a while. And the full-year outcomes had been nearly precisely what I anticipated.

I noticed Diploma’s report final month and anticipated Halma’s to be comparable. What I didn’t predict was the inventory market’s response.

I’m not satisfied that Halma and Diploma are as totally different as buyers think about. So I’m going to take one other take a look at the inventory within the subsequent few days.

Must you make investments £5,000 in Halma Plc proper now?

When investing knowledgeable Mark Rogers and his crew have a inventory tip, it may well pay to hear. In any case, the flagship Twelfth Magpie Share Advisor e-newsletter he has run for practically a decade has supplied hundreds of paying members with prime inventory suggestions from the UK and US markets.

And proper now, Mark thinks there are 6 standout shares that buyers ought to contemplate shopping for. Need to see if Halma Plc made the checklist?

Stephen Wright owns shares in Apple and Berkshire Hathaway.

Picture supply: Getty Photographs

Halma (LSE:HLMA) has been certainly one of my prime FTSE 100 development shares for a while. However the inventory crashed 14% on Thursday (11 June) after the agency launched its full-year earnings.

Is that this my alternative? Or has one thing gone badly improper with one of many UK’s prime long-term compounders of the final 10 years?

What’s occurred?

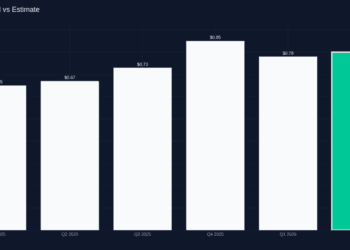

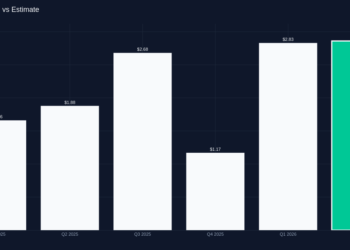

Halma’s full-year replace reported 16.6% natural income development. And – as I predicted – it’s been 12 months for the photonics division.

This sells tools to information centres, the place demand has clearly been large. Consequently, this a part of the enterprise grew 52%.

Seeing this coming wasn’t particularly arduous work. Diploma – one other FTSE 100 firm – posted largely comparable outcomes not too long ago.

The factor is, buyers cheered Diploma’s announcement prefer it was a hero. However the response to Halma has been fairly totally different.

Apparently, when Diploma sells to information centres, it’s a masterclass. When Halma does it, it’s a cyclical tightrope stroll.

Is that proper? Or is the market’s uneven response an enormous alternative for me to purchase a inventory I’ve had my eye on for some time?

What’s to not like?

Buyers reacted negatively to Halma’s information for 2 causes. The primary is focus.

The agency revealed that its photonics enterprise sells to a single information centre buyer. And that makes up round 20% of its total income.

It additionally accounted for round half of the overall natural development. So development elsewhere within the enterprise was fairly modest.

| Division | Natural Progress |

|---|---|

| Security | 5.9% |

| Environmental & Evaluation | 33.60% |

| Healthcare | 4.90% |

The opposite difficulty is cyclicality. Administration warned that photonics development is more likely to sluggish to 30% subsequent 12 months. That’s nonetheless loads, nevertheless it’s decrease.

Diploma’s report didn’t announce both of those points. The demand difficulty, nonetheless, is more likely to be the identical for each firms.

The focus threat is actual. However buyers shouldn’t overlook the place this obvious downside has come from.

Lengthy-term power

Halma acquired Avo Photonics in 2011 at a modest worth when it was a tiny fraction of its present measurement. And that transfer has labored out spectacularly.

It jogs my memory a little bit of Warren Buffett’s Apple funding. That labored out so properly that it got here to dominate Berkshire Hathaway’s portfolio.

Buyers ought to need Halma to do offers like this so what they need to hope for is extra of the identical.

There are optimistic indicators on this entrance. Within the final 12 months, the agency invested a file £447m and two extra have been accomplished for the reason that finish of the 12 months.

That’s a key long-term power for Halma. It’s an enormous a part of why the inventory has been such funding during the last 10 years.

This isn’t to say buyers ought to ignore the focus threat. However they need to keep in mind why it’s come about.

Is that this my alternative?

Halma is a inventory I’ve had on my radar for a while. And the full-year outcomes had been nearly precisely what I anticipated.

I noticed Diploma’s report final month and anticipated Halma’s to be comparable. What I didn’t predict was the inventory market’s response.

I’m not satisfied that Halma and Diploma are as totally different as buyers think about. So I’m going to take one other take a look at the inventory within the subsequent few days.

Must you make investments £5,000 in Halma Plc proper now?

When investing knowledgeable Mark Rogers and his crew have a inventory tip, it may well pay to hear. In any case, the flagship Twelfth Magpie Share Advisor e-newsletter he has run for practically a decade has supplied hundreds of paying members with prime inventory suggestions from the UK and US markets.

And proper now, Mark thinks there are 6 standout shares that buyers ought to contemplate shopping for. Need to see if Halma Plc made the checklist?

Stephen Wright owns shares in Apple and Berkshire Hathaway.

{kind=link}