Picture supply: Getty Photographs

Analysts from banks and brokers put out their view on FTSE corporations, together with a 12-month goal value. Despite the fact that it’s not at all times right, bearing in mind the common goal value from a large number of specialists can present a superb gauge on sentiment round a selected firm. So what’s the story behind the share I’m immediately?

I’m speaking about Gamma Communications (LSE:GAMA). Over the previous 12 months, the inventory’s down 32%, but it’s nonetheless within the FTSE 250. As such, it’s not a small inventory that we’re speaking about for doubtlessly giant good points.

The share value is at present 899p. I can see 11 totally different contributors to the forecast, with the bottom at 1,080p and the very best at 1,820p. A notable point out goes to Barclays, with the staff forecasting a value subsequent 12 months of 1,600p.

Based mostly on the common goal value of 1,483p, if hit, this could imply a 65% improve from the present degree. Even when this common isn’t reached, even the bottom anticipated value is larger than the place the UK inventory is true now.

Taking a step again

Earlier than I get into my view, it’s necessary to know why the inventory has fallen over the previous 12 months. A 32% drop isn’t one thing that may be dismissed!

The enterprise is a cloud telephony supplier that sells associated expertise and software program. Sadly, demand amongst small companies has been weaker resulting from financial circumstances, dampening natural income development.

Additional, there’s a present structural shift within the trade associated to the UK PSTN switch-off. This course of, which entails ending the outdated copper telephone community, has been delayed and has lowered short-term earnings. It’s because prospects changing outdated {hardware} with fibre options typically generate decrease revenue margins for Gamma.

Despite the fact that these stay dangers going ahead, an replace final month confirmed that adjusted EBITDA for the complete 12 months is predicted to fall throughout the consensus vary of £140m to £143m. Subsequently, the enterprise continues to be worthwhile and doing properly, simply not on the tempo of development some anticipate.

Nicely-positioned

There are many causes to assume the inventory might do properly within the coming 12 months. The broader shift to cloud communications continues. Gamma is properly positioned to learn from this ongoing transfer. It’s additionally seeing sturdy development within the German market, and numerous companies there aren’t absolutely on cloud communications, presenting a profitable alternative.

But whereas I imagine the inventory might rally in 2026, I battle to see the potential for a 65% surge. The place would that comes from? Nonetheless, I do assume the corporate seems like good worth after the worth fall, so it’s a inventory to contemplate for buyers. From there, the extent of its rebound is anyone’s guess!

Picture supply: Getty Photographs

Analysts from banks and brokers put out their view on FTSE corporations, together with a 12-month goal value. Despite the fact that it’s not at all times right, bearing in mind the common goal value from a large number of specialists can present a superb gauge on sentiment round a selected firm. So what’s the story behind the share I’m immediately?

I’m speaking about Gamma Communications (LSE:GAMA). Over the previous 12 months, the inventory’s down 32%, but it’s nonetheless within the FTSE 250. As such, it’s not a small inventory that we’re speaking about for doubtlessly giant good points.

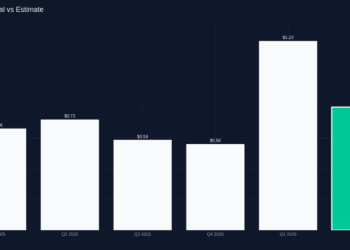

The share value is at present 899p. I can see 11 totally different contributors to the forecast, with the bottom at 1,080p and the very best at 1,820p. A notable point out goes to Barclays, with the staff forecasting a value subsequent 12 months of 1,600p.

Based mostly on the common goal value of 1,483p, if hit, this could imply a 65% improve from the present degree. Even when this common isn’t reached, even the bottom anticipated value is larger than the place the UK inventory is true now.

Taking a step again

Earlier than I get into my view, it’s necessary to know why the inventory has fallen over the previous 12 months. A 32% drop isn’t one thing that may be dismissed!

The enterprise is a cloud telephony supplier that sells associated expertise and software program. Sadly, demand amongst small companies has been weaker resulting from financial circumstances, dampening natural income development.

Additional, there’s a present structural shift within the trade associated to the UK PSTN switch-off. This course of, which entails ending the outdated copper telephone community, has been delayed and has lowered short-term earnings. It’s because prospects changing outdated {hardware} with fibre options typically generate decrease revenue margins for Gamma.

Despite the fact that these stay dangers going ahead, an replace final month confirmed that adjusted EBITDA for the complete 12 months is predicted to fall throughout the consensus vary of £140m to £143m. Subsequently, the enterprise continues to be worthwhile and doing properly, simply not on the tempo of development some anticipate.

Nicely-positioned

There are many causes to assume the inventory might do properly within the coming 12 months. The broader shift to cloud communications continues. Gamma is properly positioned to learn from this ongoing transfer. It’s additionally seeing sturdy development within the German market, and numerous companies there aren’t absolutely on cloud communications, presenting a profitable alternative.

But whereas I imagine the inventory might rally in 2026, I battle to see the potential for a 65% surge. The place would that comes from? Nonetheless, I do assume the corporate seems like good worth after the worth fall, so it’s a inventory to contemplate for buyers. From there, the extent of its rebound is anyone’s guess!

{kind=link}