Shares of Lamb Weston Holdings, Inc. (NYSE: LW) stayed inexperienced on Tuesday. The inventory has dropped 27% prior to now three months. The frozen potato merchandise maker continues to function in a fluid and aggressive atmosphere and has been battling just a few headwinds. Nevertheless, the corporate has been specializing in what it could possibly management and this has helped it make progress in sure areas of its enterprise.

Gross sales and quantity progress towards value/combine challenges

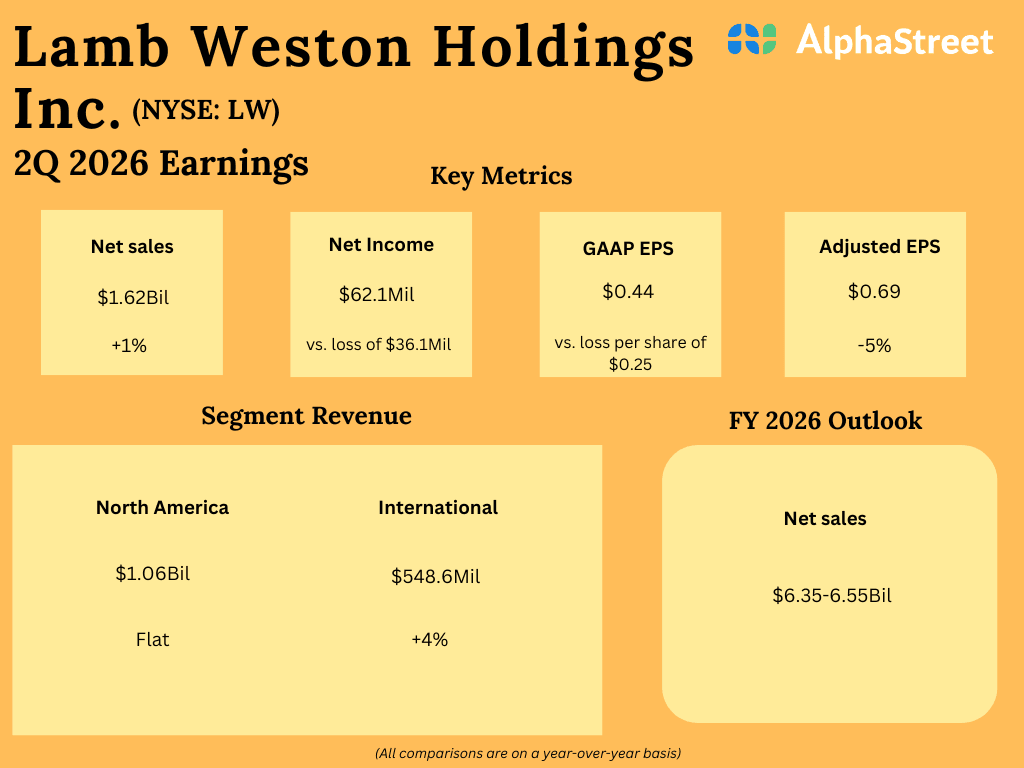

Lamb Weston’s internet gross sales rose 1% to $1.62 billion within the second quarter of 2026 in comparison with the earlier 12 months. Quantity elevated 8%, pushed by buyer wins, share beneficial properties and robust retention, significantly in North America and Asia. The corporate continued to realize share even with new and rising clients and this helped it develop quantity regardless of softness in restaurant visitors.

As talked about on the Q2 earnings name, QSR, or quick-service restaurant, visitors within the US remained flat through the three-month interval of August, September and October, with progress in QSR hen and declines in QSR burger. French fry quantity in North America foodservice gained barely, reflecting resilient demand. Restaurant visitors in most worldwide markets declined, with the most important market, the UK, witnessing a 3% drop.

Lamb Weston’s quantity progress in Q2 was offset by a decline in value/combine. Value/combine fell 8%, attributable to impacts from pricing and commerce to assist clients, in addition to combine shifts in direction of lower-margin gross sales. The impression from unfavorable value/combine led to a lower in adjusted gross revenue, which in flip brought on earnings per share, on an adjusted foundation, to say no 5% year-over-year to $0.69.

Value/combine declined throughout the corporate’s enterprise segments as nicely through the second quarter, and is anticipated to stay unfavorable within the second half of the 12 months though to a lesser extent than the primary half.

Steady North America enterprise and Worldwide growth

Lamb Weston’s North America enterprise phase stays steady. In Q2, internet gross sales of $1.07 billion had been flat year-over-year, however quantity grew 8%, pushed by buyer contract wins, share beneficial properties, and progress throughout channels. The corporate additionally restarted its beforehand curtailed manufacturing strains in North America to keep up its excessive service ranges.

LW is meaningfully increasing its worldwide presence. Internet gross sales within the Worldwide phase elevated 4% to $548.6 million within the second quarter versus the earlier 12 months. Quantity grew 7%, helped by progress in Asia and with multinational chain clients.

The corporate’s international manufacturing footprint and provide chain community can assist construct buyer partnerships that may permit it to seize quantity in fast-growing markets comparable to Asia and Latin America. Its new facility in Argentina has began manufacturing and with the speedy progress within the area, the French fry maker sees alternative for significant share beneficial properties.

Nevertheless, worldwide markets stay aggressive. In Q2, LW confronted softness in restaurant visitors, decrease export demand, and pricing pressures in Europe. The corporate expects to proceed supporting clients with value and commerce by way of fiscal 12 months 2026.

Outlook

Lamb Weston expects sturdy gross sales and quantity for the rest of fiscal 12 months 2026. North America is anticipated to see volumes within the second half develop at or above first-half charges, helped by sturdy demand. Worldwide volumes are anticipated to be flat as the corporate laps prior-year buyer wins. LW expects internet gross sales to vary between $6.35-6.55 billion in FY2026.

{kind=link}