Shares of The J.M. Smucker Co. (NYSE: SJM) plunged 15% on Tuesday after the corporate delivered blended outcomes for the fourth quarter of 2025. Whereas earnings got here forward of expectations, revenues fell brief. The branded meals supplier anticipates a dynamic working atmosphere in fiscal 12 months 2026 with possible impacts from tariffs, enter inflation and shifts in shopper conduct.

Combined outcomes

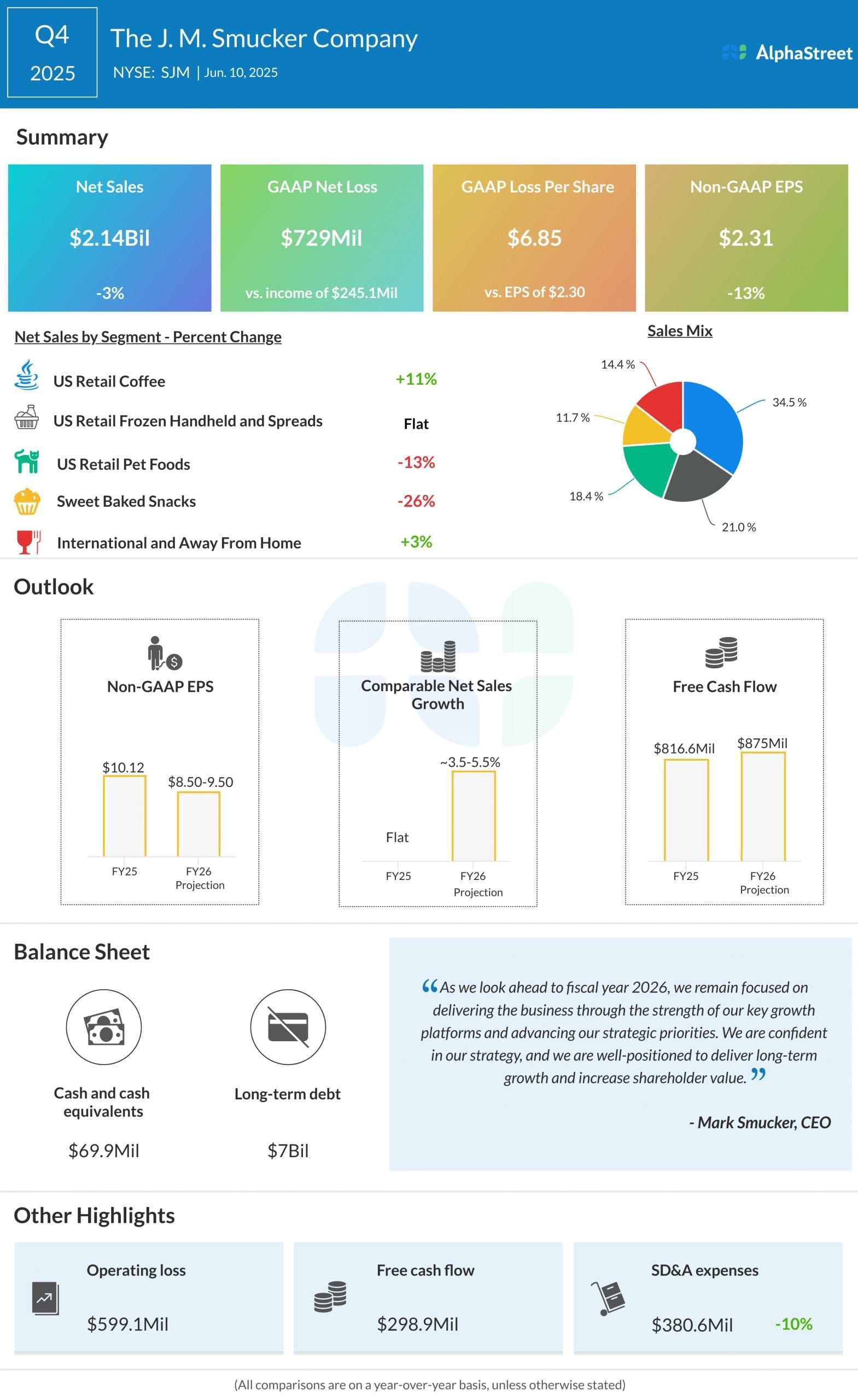

Within the fourth quarter of 2025, JM Smucker’s web gross sales decreased 3% year-over-year to $2.14 billion, lacking estimates of $2.19 billion. On a GAAP foundation, the corporate reported a web lack of $6.85 per share. Adjusted earnings per share fell 13% YoY to $2.31 however surpassed analysts’ expectations of $2.25.

Enterprise efficiency

In This fall, gross sales within the Espresso section elevated 11%, primarily pushed by value will increase for the Folgers and Café Bustelo manufacturers. SJM continues to see inflation in inexperienced espresso and after rolling out two value will increase final fiscal 12 months, it’s engaged on implementing two extra this 12 months. Because of this, it anticipates some value elasticity of demand influence to quantity. The corporate additionally expects continued resilience within the at-home espresso class.

Gross sales remained flat within the Frozen Handheld and Spreads section, with the Uncrustables sandwiches model sustaining its progress whereas Smucker’s fruit spreads and Jif peanut butter noticed declines. Pet Meals section gross sales dropped 13% with stress within the canine snacks class brought on by decrease discretionary spend and inflationary pressures. SJM continued to see progress within the cat meals class helped by its Meow Combine model.

The Candy Baked Snacks section continues to be impacted by inflationary pressures and lowered discretionary spend together with weak point within the comfort channel. Gross sales for this section decreased 26% in This fall.

SJM continues to focus its assets on key manufacturers resembling Uncrustables, Café Bustelo, Meow-Combine, Milk-Bone, and Hostess, the place it sees the most important alternative for progress. The Uncrustables model continues to see robust momentum with product innovation and manufacturing growth. The corporate plans to broaden this model into the comfort channel to drive additional progress. The Uncrustables model is on monitor to generate over $1 billion in gross sales by the tip of fiscal 12 months 2026.

The Café Bustelo model is without doubt one of the fastest-growing manufacturers within the at-home espresso class and it’s benefiting from product innovation. The corporate anticipates double-digit gross sales progress for this model within the coming 12 months. The Meow-Combine and Milk-Bone manufacturers are anticipated to learn from product innovation and the pet humanization pattern.

Outlook

Looking forward to fiscal 12 months 2026, JM Smucker expects a dynamic working atmosphere impacted by tariffs, excessive inexperienced espresso prices, coverage modifications, and value-seeking prospects. The corporate expects web gross sales progress of 2-4% and comparable gross sales progress of three.5-5.5% for FY2026. SJM anticipates the very best influence from tariffs to be on inexperienced espresso. Adjusted EPS is predicted to be $8.50-9.50.

Within the first quarter of 2026, web gross sales are anticipated to say no low-single-digits, comparable gross sales are anticipated to stay flat, and adjusted EPS is predicted to say no approx. 25%.

{kind=link}