Bitcoin miners’ identification is fracturing on 4 fronts concurrently: crushed margins, accelerating AI pivots, increasing debt masses, and a treasury promote self-discipline that not holds.

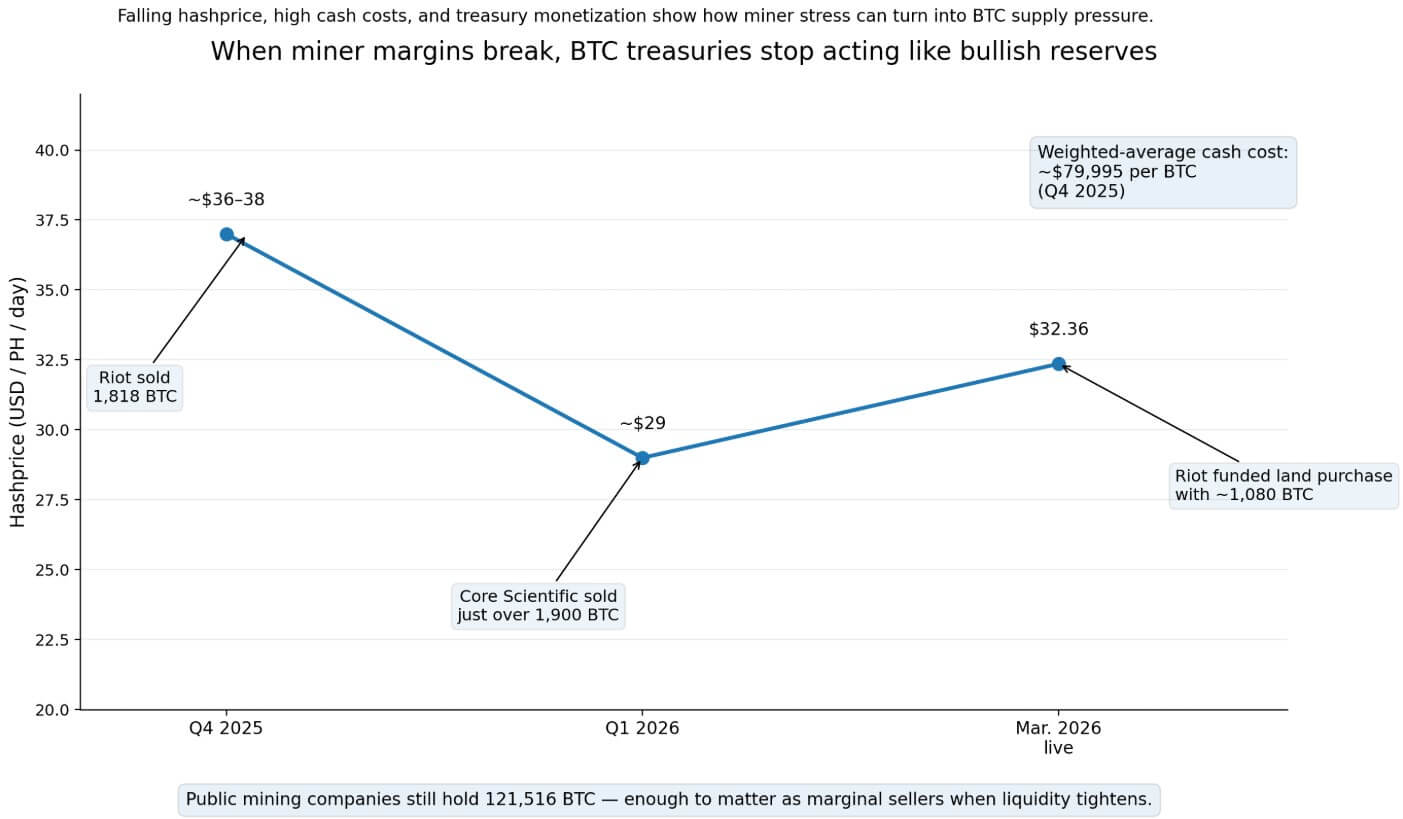

CoinShares’ newest mining report exhibits public miners’ weighted-average money price was roughly $79,995 per BTC within the fourth quarter of 2025. The hash worth fell to roughly $36-$38 per PH/s/day in the identical quarter, then dropped additional to round $29 within the first quarter of 2026.

The community logged three consecutive unfavorable issue changes, the primary such streak since July 2022. The stay hash worth at the moment sits round $32.36/PH/day, with charges at simply 0.40% of block rewards, and the six-month ahead market common hash worth is close to $30.42.

What miners do below these circumstances is the place the market construction case begins.

Public mining firms collectively maintain 121,516 BTC, value roughly $8.63 billion, making them significant marginal sellers, even after dropping their standing because the dominant public-company treasury class.

A number of have already moved from holding to promoting. MARA modified its technique in 2025 to allow gross sales of Bitcoin from operations and expanded that in 2026 to incorporate stability sheet BTC.

Riot Platforms bought 1,818 BTC in December 2025 for $161.6 million, Core Scientific bought simply over 1,900 BTC in January 2026 for about $175 million, and now holds below 1,000 BTC.

Riot individually funded a 200-acre land buy at Rockdale fully by promoting roughly 1,080 BTC from its stability sheet.

That conduct runs counter to a persistent retail assumption that miners maintain by default and that enormous miner treasury balances are structurally bullish.

When margins break, miners act like commodity producers managing liquidity, and Treasury coverage turns into pro-cyclical, with promoting concentrated exactly when BTC is already weak.

The identification break up

The fracture described by CoinShares runs deepest via the AI pivot.

The agency says listed miners might derive as much as 70% of their revenues from AI by the tip of 2026, up from roughly 30% at the moment.

Core Scientific has energized about 350 MW for CoreWeave and targets roughly 590 MW by early 2027. Its income within the fourth quarter of 2025 already confirmed $42.2 million from self-mining, versus $31.3 million from colocation.

Hut 8 signed a 15-year, 245 MW AI knowledge heart lease with a $7 billion base-term worth. IREN reported $17.3 million in AI Cloud Providers income, secured $3.6 billion of GPU financing tied to a Microsoft contract, and guides buyers towards a $3.4 billion ARR goal by end-2026.

TeraWulf says it has signed greater than $12.8 billion in long-term buyer contracts and accomplished $6.5 billion in long-term financings in 2025. Riot signed its first AMD data-center lease.

For fairness buyers, that redefines what a miner inventory truly represents. Shopping for a listed miner now bundles publicity to BTC worth, hyperscaler demand, lease execution timelines, retrofit capital expenditure, financing prices, and counterparty high quality.

CoinShares described this explicitly as a bifurcation, with AI/HPC-linked names incomes valuation premiums over pure-play miners. The shares share the identical ticker symbols, whereas the underlying companies have shifted their facilities of gravity.

| Firm | Mining enterprise sign | AI/HPC sign | Debt / financing sign | What the inventory more and more represents |

|---|---|---|---|---|

| Core Scientific | $42.2M self-mining income | $31.3M colocation income; 350 MW energized; 590 MW goal | Expanded financing facility | Hybrid mining + data-center execution |

| Hut 8 | Nonetheless mines BTC | 245 MW, 15-year AI lease | Massive long-term infrastructure publicity | Energy + digital infrastructure platform |

| IREN | Mining stays significant | $17.3M AI cloud income; $3.4B ARR goal | ~$3.7B convertible notes | Levered AI + mining hybrid |

| TeraWulf | Mining nonetheless current | $12.8B buyer contracts | Heavy financing and debt | AI landlord with mining residual |

| Riot | Mining-led model | AMD data-center lease | Treasury monetization + growth capex | BTC publicity plus data-center optionality |

| Cipher | Mining operator | HPC diversification below improvement | Multi-billion secured notes | Leverage-heavy transition story |

Debt load amplifies that divergence. IREN carries practically $3.7 billion of convertible notes payable as of Dec. 31, 2025. TeraWulf’s stability sheet exhibits roughly $46.3 million in present long-term debt, $489.8 million in short-term convertibles, $3.05 billion in long-term debt, and $1.58 billion in convertible notes.

Core Scientific expanded its strategic financing facility to $1 billion. Cipher disclosed $3.73 billion in current senior secured word financing.

Companies constructed round these stability sheets care about charges, refinancing home windows, build-cost inflation, and buyer focus in ways in which pure Bitcoin miners by no means needed to.

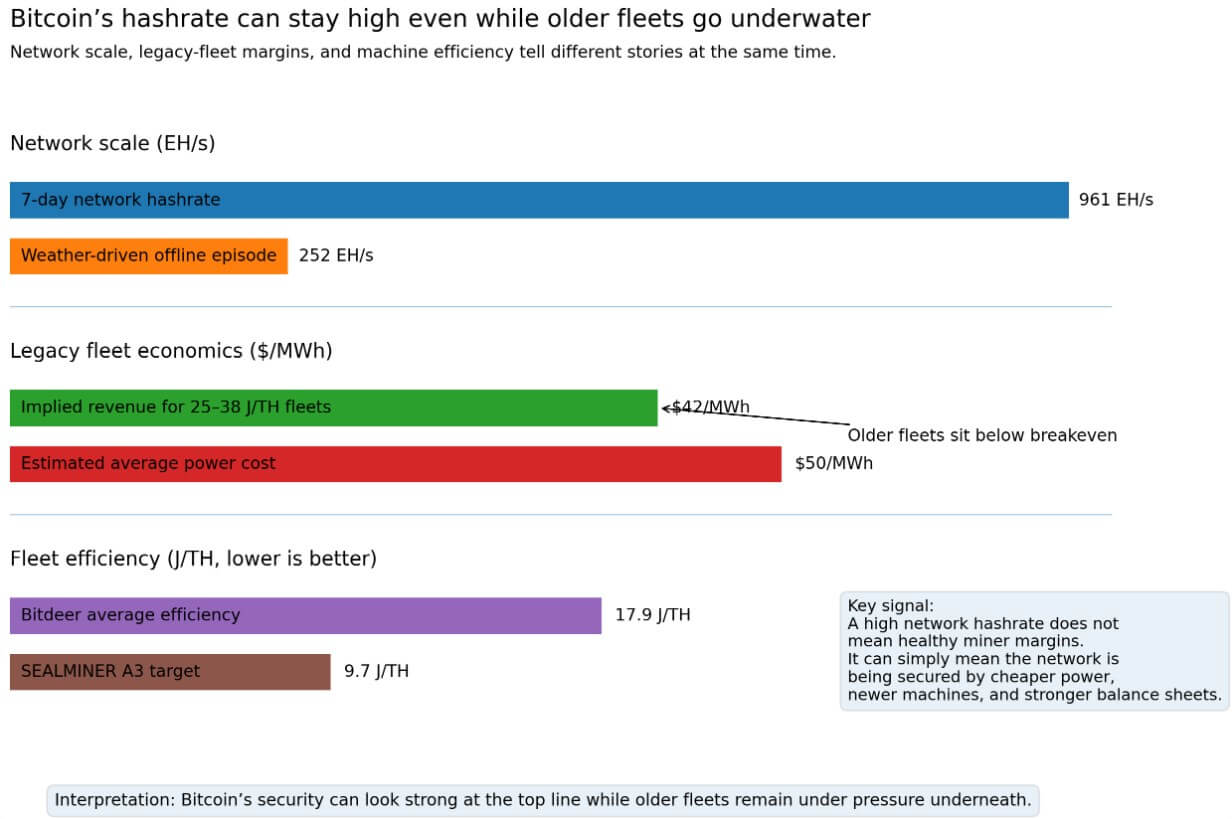

In the meantime, community hashrate runs at roughly 961 EH/s, a determine the Luxor knowledge places in sharper context.

Fleets working at 25–38 J/TH have been incomes about $42/MWh in implied income in opposition to an estimated network-average energy price of $50/MWh, leaving S19-class {hardware} in unfavorable gross-margin territory all through February.

Luxor additionally documented a 252 EH/s weather-driven offline episode, exhibiting how rapidly marginal fleets disappear when economics tighten.

Bitdeer achieved a median miner effectivity of 17.9 J/TH within the fourth quarter of 2025 and is concentrating on 9.7 J/TH with its SEALMINER A3.

A excessive hashrate can now coexist with widespread unprofitability in older fleets, that means a narrower, better-capitalized, extra machine-efficient survivor set now secures the community. On the identical time, the broader sector stays below pressure.

Potential eventualities

If BTC recovers towards the $100,000 vary, hash worth eases, and rapid treasury stress lifts, the fairness winners are the operators that may pair recovering mining margins with credible AI/HPC execution, as a result of these names seize each the BTC restoration and an infrastructure rerating.

Core, Riot, Hut 8, TeraWulf, and IREN all have enough disclosed knowledge heart ambitions to drive worth restoration and widen the hole between hybrid and pure-play names.

In that situation, the AI pivot transforms from a survival technique right into a valuation catalyst, and probably the most debt-loaded operators with the strongest contract pipelines earn multiples that pure miners can’t match.

If BTC stays beneath the stress thresholds CoinShares flagged, hash worth holds within the high-$20s to low-$30s, and extra treasury drawdowns normalize throughout the sector.

Luxor’s February fleet knowledge suggests many legacy machines have been already underwater earlier than any additional worth decline, so {that a} sustained downturn would speed up compelled shutdowns, reserve monetization, and a switch of shares towards low-cost, next-generation operators.

The sector’s mixed 121,516 BTC in treasuries turns into a provide overhang that prompts exactly when BTC spot markets are softest.

On the identical time, miners carrying multi-billion-dollar convertible masses face refinancing stress if AI contract execution slips or capital markets tighten.

Essentially the most debt-loaded hybrids then soak up headwinds from two instructions concurrently: BTC worth and infrastructure construct credibility.

The fracture CoinShares’ report paperwork runs beneath each eventualities.

Miners not share a unified BTC appreciation thesis, and a few at the moment are promoting BTC to fund operations.

Some derive extra enterprise worth from data-center lease execution than from block rewards.

Some profit from Bitcoin’s weak spot solely as soon as weaker rivals shut down, and the problem eases, releasing up margin for the survivors.

The businesses nonetheless securing Bitcoin’s blocks are splitting into compelled commodity sellers, debt-funded AI landlords, and a thinning cohort of environment friendly pure-play operators with the facility prices and machine high quality to outlive with out pivoting.

{kind=link}