For Johnson & Johnson (NYSE: JNJ), 2025 has been a robust yr, marked by a powerful monetary efficiency that drove the inventory sharply increased mid-year. Buyers can be retaining a detailed watch on the healthcare behemoth’s third-quarter earnings to verify the way it offers with macroeconomic challenges. Latest investor optimism additionally displays the corporate’s restricted publicity to pharma tariffs, with its important US investments anticipated to cushion the influence of import taxes on patented medicine.

Robust Q3 in Playing cards

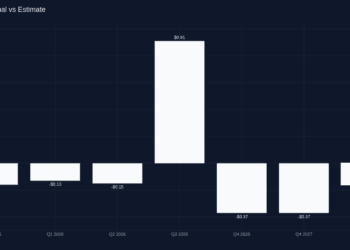

Johnson & Johnson will publish its third-quarter FY26 earnings report on Tuesday, October 14, at 6.20 am ET. Market watchers forecast a 14% year-over-year enhance in adjusted earnings to $2.75 per share. Their consensus income forecast for Q3 is $23.73 billion, up 5.6% from final yr’s third quarter. The corporate has earned the uncommon distinction of constantly delivering stronger-than-expected quarterly earnings for over a decade.

The inventory has gained about 29% in 2025, often outperforming the broader market and reaching an all-time excessive this week. It ranks among the many top-performing healthcare shares within the S&P 500. Regardless of the comparatively excessive valuation, JNJ seems to be a compelling funding, given the corporate’s sturdy observe report of rewarding buyers even whereas going through challenges. JNJ has been a favourite amongst long-term buyers — the diversified enterprise mannequin and common dividend hikes make it a lovely wager.

But One other Beat

Within the second quarter of fiscal 2025, gross sales totaled $23.7 billion, up 5.8% year-over-year. Operational gross sales rose 4.6% within the June quarter. In the meantime, Q2 adjusted earnings, excluding particular gadgets, declined 1.8% YoY to $2.77 per share. On a reported foundation, web revenue was $5.5 billion or $2.29 per share, up 18% from the comparable quarter of fiscal 2024. Each the highest line and earnings beat Wall Road’s expectations. Presently, the main target of Johnson & Johnson’s pipeline and portfolio technique is on six areas of unmet want and the place the corporate is delivering sturdy progress — oncology, immunology, neuroscience, cardiovascular, surgical procedure, and imaginative and prescient.

From Johnson & Johnson’s Q2 2025 Earnings Name:

“We proceed to advance our pipeline, attaining important medical and regulatory milestones that may assist drive sustained and accelerating progress by means of the again half of the last decade. In MedTech, whereas we nonetheless have work to do, we noticed enchancment over first-quarter outcomes. Pushed by sturdy efficiency within the cardiovascular portfolio, surgical imaginative and prescient, and wound closure in surgical procedure. We stay centered on higher-growth markets, enhancing competitiveness to realize market share, and executing in opposition to our transformation initiatives to enhance margins.“

Street Forward

Inspired by the spectacular efficiency throughout the Progressive Drugs and MedTech enterprise segments, in addition to favorable international change charges, the Johnson & Johnson management raised its full-year gross sales steerage to vary between $93.2 billion and $93.6 billion. It additionally revised up the adjusted earnings forecast to the vary of $10.80 per share to $10.90 per share. The corporate bets on its diversified portfolio and pipeline to ship sturdy progress within the second half, whereas anticipating main regulatory approvals in a number of healthcare areas, together with oncology, main depressive dysfunction, and psoriasis.

Prior to now two-and-a-half months, shares of Johnson & Johnson have constantly traded above their 52-week common worth of $159.39. The inventory traded up 1.5% on Friday morning, after closing the final session at an all-time excessive.

{kind=link}