Picture supply: M&S Group plc

Marks and Spencer (LSE: MKS) shares have risen by round 20% during the last month, making the agency one of many high performers within the FTSE 100 over this era.

The retailer’s shares have climbed by practically 60% during the last 12 months. On a five-year view, the M&S share worth has risen by a powerful 350%.

On this piece I’m asking whether or not traders ought to nonetheless think about shopping for M&S shares. Is there nonetheless extra to return from this spectacular turnaround?

Sturdy momentum

A number of years in the past, Marks and Spencer appeared an unlikely alternative for an funding success story. Falling gross sales, dated inventory, and unprofitable shops had been holding again income.

Since CEO Stuart Machin took cost in Might 2022, a lot of this has modified. Annual gross sales have risen by 23% to £13.4bn, whereas working revenue is up by nearly 50% to £864m.

Machin has reduce debt, closed unprofitable shops, and led a revamp of the core Clothes, Dwelling & Magnificence enterprise. On the similar time, M&S Meals has continued to carve out a distinct segment as a well-liked alternative for customers searching for an inexpensive improve from the large supermarkets.

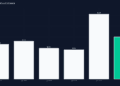

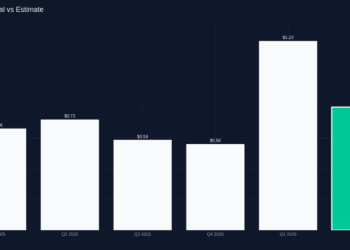

The corporate’s most up-to-date buying and selling replace lined the final 13 weeks of 2024 – together with the all-important Christmas interval. Whole group gross sales rose by 5.6% to £4.1bn.

Meals gross sales had been up by 8.7%, together with the “greatest day” ever.

In the meantime, the group’s Clothes, Dwelling & Magnificence division achieved its greatest ever week of on-line gross sales.

Is a slowdown doubtless?

I believe there are some good causes to take a extra cautious view on M&S shares. To begin with, this enterprise is just not as low cost because it was.

As I write, the shares are buying and selling on round 13 instances 2025/26 forecast earnings. A 12 months in the past, Marks and Spencer’s forecast price-to-earnings ratio (P/E) was solely 10.

A P/E of 13 isn’t costly for all sorts of enterprise. However M&S is a big, mature retailer working in a sluggish UK economic system. Revenue margins are comparatively low.

Development during the last couple of years has been boosted by operational enhancements. With many of those adjustments now full, I’m not positive if latest progress charges can be sustainable. Slowing progress might put stress on the inventory’s valuation.

There’s additionally the danger that new issues might hit the enterprise. On 22 April, M&S revealed that its retailer operations had been hit by a latest cyberattack. In line with some press stories, click on and accumulate companies had been disrupted.

The corporate hasn’t revealed any particulars concerning the assault. However occasions reminiscent of this may be pricey and take time to resolve.

M&S shares: purchase or keep away from?

All investments carry some threat. However I believe there are some good causes to stay optimistic about Marks & Spencer. This enterprise has an enormous footprint in UK retail and is working rather more competitively than it was a couple of years in the past.

On-line progress can be a optimistic. Many consumers count on a seamless mix of in-store and on-line retail, and M&S is nicely positioned to offer this.

In the meantime, the M&S Meals enterprise might do nicely, even in a recession, as customers purchase treats to eat at house as a substitute of eating out.

Total, I believe M&S remains to be value contemplating as a doable funding.

Picture supply: M&S Group plc

Marks and Spencer (LSE: MKS) shares have risen by round 20% during the last month, making the agency one of many high performers within the FTSE 100 over this era.

The retailer’s shares have climbed by practically 60% during the last 12 months. On a five-year view, the M&S share worth has risen by a powerful 350%.

On this piece I’m asking whether or not traders ought to nonetheless think about shopping for M&S shares. Is there nonetheless extra to return from this spectacular turnaround?

Sturdy momentum

A number of years in the past, Marks and Spencer appeared an unlikely alternative for an funding success story. Falling gross sales, dated inventory, and unprofitable shops had been holding again income.

Since CEO Stuart Machin took cost in Might 2022, a lot of this has modified. Annual gross sales have risen by 23% to £13.4bn, whereas working revenue is up by nearly 50% to £864m.

Machin has reduce debt, closed unprofitable shops, and led a revamp of the core Clothes, Dwelling & Magnificence enterprise. On the similar time, M&S Meals has continued to carve out a distinct segment as a well-liked alternative for customers searching for an inexpensive improve from the large supermarkets.

The corporate’s most up-to-date buying and selling replace lined the final 13 weeks of 2024 – together with the all-important Christmas interval. Whole group gross sales rose by 5.6% to £4.1bn.

Meals gross sales had been up by 8.7%, together with the “greatest day” ever.

In the meantime, the group’s Clothes, Dwelling & Magnificence division achieved its greatest ever week of on-line gross sales.

Is a slowdown doubtless?

I believe there are some good causes to take a extra cautious view on M&S shares. To begin with, this enterprise is just not as low cost because it was.

As I write, the shares are buying and selling on round 13 instances 2025/26 forecast earnings. A 12 months in the past, Marks and Spencer’s forecast price-to-earnings ratio (P/E) was solely 10.

A P/E of 13 isn’t costly for all sorts of enterprise. However M&S is a big, mature retailer working in a sluggish UK economic system. Revenue margins are comparatively low.

Development during the last couple of years has been boosted by operational enhancements. With many of those adjustments now full, I’m not positive if latest progress charges can be sustainable. Slowing progress might put stress on the inventory’s valuation.

There’s additionally the danger that new issues might hit the enterprise. On 22 April, M&S revealed that its retailer operations had been hit by a latest cyberattack. In line with some press stories, click on and accumulate companies had been disrupted.

The corporate hasn’t revealed any particulars concerning the assault. However occasions reminiscent of this may be pricey and take time to resolve.

M&S shares: purchase or keep away from?

All investments carry some threat. However I believe there are some good causes to stay optimistic about Marks & Spencer. This enterprise has an enormous footprint in UK retail and is working rather more competitively than it was a couple of years in the past.

On-line progress can be a optimistic. Many consumers count on a seamless mix of in-store and on-line retail, and M&S is nicely positioned to offer this.

In the meantime, the M&S Meals enterprise might do nicely, even in a recession, as customers purchase treats to eat at house as a substitute of eating out.

Total, I believe M&S remains to be value contemplating as a doable funding.

{kind=link}