Moody’s Company (MCO) remains to be typically framed as a simple guess on debt-market exercise. That view captures an vital a part of the story, as a result of Moody’s Traders Service (MIS) earns extremely worthwhile charges when bond and structured-finance issuance is robust. Nevertheless it now not captures the entire enterprise. The higher approach to consider Moody’s in the present day is as a two-engine mannequin: a recurring workflow and knowledge franchise in Moody’s Analytics (MA), paired with a rankings enterprise that may add substantial working leverage when capital markets are open.

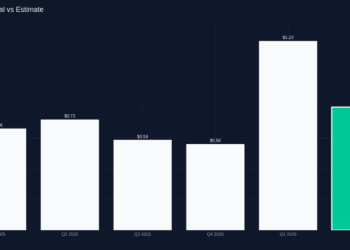

That distinction issues as a result of it modifications how buyers ought to take into consideration sturdiness throughout the cycle. In FY2025, Moody’s generated $7.718 billion in income, with roughly $3.6 billion from MA and about $4.1 billion from MIS. In Q1 2026, that blend continued to point out why the corporate is extra resilient than a pure rankings store. MA income rose 8% to $926 million, though MA transaction income fell 54% 12 months over 12 months, whereas MIS posted file first-quarter income of $1.153 billion on greater than $2 trillion in rated issuance. The lesson isn’t that Moody’s has develop into non-cyclical. It’s that one a part of the corporate now gives a a lot steadier base than the market’s previous template assumes.

Why Moody’s is not only a debt-issuance proxy

If buyers look solely at issuance volumes, they’ll miss the structural change inside Moody’s. The corporate nonetheless advantages meaningfully from wholesome credit score markets. That was apparent in FY2025, when MIS had a file 12 months as rated issuance topped $6.6 trillion and the phase’s adjusted working margin reached 63.6%. It was simply as seen in Q1 2026, when MIS delivered file first-quarter income and a 66.7% adjusted working margin.

However Moody’s is not only MIS anymore. MA has develop into a big subscription-led enterprise with recurring income embedded in buyer workflows. That modifications the form of consolidated earnings. In Q1 2026, companywide income elevated 8% to $2.079 billion, adjusted working margin improved to 53.2% from 51.7%, working money movement rose to $939 million from $757 million, and free money movement climbed to $844 million from $672 million. These figures replicate an organization with multiple driver.

The only approach to body Moody’s now could be this: MIS stays the cyclical torque, however MA more and more provides the bottom load. That may be a higher psychological mannequin than treating all of Moody’s as a clear read-through on company bond home windows, refinancing exercise, or unfold sentiment.

What MA’s recurring income base says about sturdiness

MA is the clearest proof that Moody’s needs to be seen by means of a broader lens. In Q1 2026, MA income elevated to $926 million from $859 million. Extra importantly, recurring income rose 11% and represented 98% of whole MA income, whereas annualized recurring income reached $3.607 billion at March 31, 2026, up from $3.343 billion a 12 months earlier. That’s the sort of income base buyers often affiliate with workflow software program, knowledge, and threat infrastructure quite than with a traditional transaction enterprise.

The stress check inside these numbers is much more revealing. MA transaction income declined 54% 12 months over 12 months in Q1 2026. In a enterprise that depended primarily on episodic challenge work, that sort of drop would possible pull the entire phase down. As a substitute, MA nonetheless grew as a result of the subscription-heavy portion of the franchise was sturdy sufficient to soak up the hit. That’s precisely what recurring income is meant to do for buyers: cut back dependence on short-term deal movement.

The sample was already seen on the finish of FY2025. MA income was about $3.6 billion for the 12 months, MA ARR was $3.498 billion at December 31, 2025 versus $3.233 billion a 12 months earlier, and MA adjusted working margin improved to 33.1%. Moody’s additionally mentioned MA recurring income comprised 97% of whole MA income in This fall 2025. That doesn’t imply MA is resistant to macro stress, competitors, or product-execution threat. It does imply that a big share of Moody’s economics now comes from recurring analytical instruments and knowledge relationships which are much less delicate to any single issuance quarter.

That recurring base additionally helps margin enchancment. MA adjusted working margin rose to 32.5% in Q1 2026 from 30.0% a 12 months earlier. For buyers, that could be a helpful sign that Moody’s is not only shopping for stability at the price of profitability. The analytics aspect is scaling.

Why MIS nonetheless drives working leverage when markets are open

None of this reduces the significance of MIS. The truth is, the rankings enterprise remains to be the primary motive Moody’s can produce outsized earnings energy in constructive markets. In Q1 2026, MIS income rose to $1.153 billion from $1.065 billion. Transaction income elevated to $790 million from $732 million, and recurring income elevated to $363 million from $333 million. That blend issues. MIS isn’t purely transaction-driven both; surveillance and associated recurring work present some continuity. However when issuance picks up, the transaction line can add high-margin income shortly.

That’s the reason the phase’s profitability is so putting. MIS adjusted working margin reached 66.7% in Q1 2026, after hitting 63.6% in FY2025. Traders don’t have to overcomplicate the takeaway: when debt markets are wholesome, MIS can convert that surroundings into very sturdy incremental earnings.

Administration’s commentary additionally reveals the place issuance demand is evolving. Moody’s mentioned Q1 2026 included file first-quarter investment-grade issuance, together with jumbo transactions and elevated AI-related financing from hyperscalers. It additionally mentioned Infrastructure Finance had its strongest quarter since 2020, helped by infrastructure funding wants and AI- and data-center-related exercise. In FY2025, Moody’s mentioned personal credit score exercise accounted for about 20% of MIS transaction income development.

These particulars shouldn’t be learn as hype factors. The extra helpful interpretation is that MIS is benefiting from a number of financing channels, not only a generic reopening in public debt markets. That broadens the chance set, even when it doesn’t eradicate cyclicality.

What buyers ought to watch subsequent: issuance high quality, regulation, and capital allocation

The principle threat to the thesis is simple: if capital markets seize up, MIS transaction income can fall sharply. Moody’s has made the consolidated mannequin extra sturdy, however it has not eliminated the cycle. That’s the reason buyers ought to watch not simply issuance quantity, however issuance combine and high quality. If present power is being supported by unusually favorable financing home windows or concentrated themes, the margin advantages in MIS might show much less sturdy than they have a look at the highest of the cycle.

Regulation stays one other actual threat. Rankings businesses function in a enterprise the place credibility, methodology, and battle administration matter as a lot as uncooked quantity. Even a well-diversified Moody’s can’t escape the potential of regulatory stress, litigation, or tighter scrutiny throughout pressured credit score durations.

Traders also needs to watch whether or not MA can maintain its present high quality of development. ARR elevated to $3.607 billion in Q1 2026, however the important thing query is whether or not that tempo can proceed whereas sustaining product relevance and wholesome retention. A recurring enterprise is sturdy provided that clients stay embedded and keen to resume.

Lastly, capital allocation deserves consideration. Moody’s returned about $1.7 billion to shareholders in Q1 2026, together with $1.5 billion in buybacks and $185 million in dividends, and it raised 2026 share repurchase steerage to about $2.5 billion from about $2.0 billion. At March 31, 2026, Moody’s had $1.469 billion in money and money equivalents, $41 million in short-term investments, and $6.387 billion in long-term debt. At year-end 2025, it had $2.384 billion in money, $64 million in short-term investments, about $7.0 billion of excellent debt, and an undrawn $1.25 billion revolving credit score facility. That isn’t a pressured stability sheet, however it does imply aggressive repurchases needs to be judged towards the identical sturdiness commonplace buyers apply to the working mannequin.

The larger image is that Moody’s now combines a recurring analytics franchise with a high-margin rankings engine. That doesn’t make it recession-proof or regulation-proof. It does make it extra sturdy than the previous one-line description of “bond-market proxy” suggests.

Key Indicators for Traders

- MA’s 98% recurring income combine in Q1 2026 suggests Moody’s has a stronger income ground than buyers often assume for a ratings-centered enterprise.

- MIS margin efficiency will stay the clearest learn on how a lot working leverage Moody’s can unlock when issuance markets keep open.

- ARR development at MA is a key sturdiness indicator; if that slows materially, the case for Moody’s as a two-engine compounder weakens.

- AI-related financing, infrastructure funding, and personal credit score are price monitoring as a result of they present the place future rankings demand might come from, not simply how a lot issuance is going on total.

- The sooner tempo of buybacks raises the significance of balance-sheet self-discipline if issuance circumstances soften.

Sources

- https://www.sec.gov/Archives/edgar/knowledge/1059556/000162828026026383/0001628280-26-026383-index.htm

- https://www.sec.gov/Archives/edgar/knowledge/1059556/000162828026026383/a1q26earningsrelease.htm

- https://www.sec.gov/Archives/edgar/knowledge/1059556/000162828026026848/mco-20260331.htm

- https://www.sec.gov/Archives/edgar/knowledge/1059556/000162828026008788/a4q25earningsrelease.htm

- https://www.sec.gov/Archives/edgar/knowledge/1059556/000162828026009136/mco-20251231.htm

All figures above are drawn from Moody’s SEC filings and official earnings releases.

Moody’s Company (MCO) remains to be typically framed as a simple guess on debt-market exercise. That view captures an vital a part of the story, as a result of Moody’s Traders Service (MIS) earns extremely worthwhile charges when bond and structured-finance issuance is robust. Nevertheless it now not captures the entire enterprise. The higher approach to consider Moody’s in the present day is as a two-engine mannequin: a recurring workflow and knowledge franchise in Moody’s Analytics (MA), paired with a rankings enterprise that may add substantial working leverage when capital markets are open.

That distinction issues as a result of it modifications how buyers ought to take into consideration sturdiness throughout the cycle. In FY2025, Moody’s generated $7.718 billion in income, with roughly $3.6 billion from MA and about $4.1 billion from MIS. In Q1 2026, that blend continued to point out why the corporate is extra resilient than a pure rankings store. MA income rose 8% to $926 million, though MA transaction income fell 54% 12 months over 12 months, whereas MIS posted file first-quarter income of $1.153 billion on greater than $2 trillion in rated issuance. The lesson isn’t that Moody’s has develop into non-cyclical. It’s that one a part of the corporate now gives a a lot steadier base than the market’s previous template assumes.

Why Moody’s is not only a debt-issuance proxy

If buyers look solely at issuance volumes, they’ll miss the structural change inside Moody’s. The corporate nonetheless advantages meaningfully from wholesome credit score markets. That was apparent in FY2025, when MIS had a file 12 months as rated issuance topped $6.6 trillion and the phase’s adjusted working margin reached 63.6%. It was simply as seen in Q1 2026, when MIS delivered file first-quarter income and a 66.7% adjusted working margin.

However Moody’s is not only MIS anymore. MA has develop into a big subscription-led enterprise with recurring income embedded in buyer workflows. That modifications the form of consolidated earnings. In Q1 2026, companywide income elevated 8% to $2.079 billion, adjusted working margin improved to 53.2% from 51.7%, working money movement rose to $939 million from $757 million, and free money movement climbed to $844 million from $672 million. These figures replicate an organization with multiple driver.

The only approach to body Moody’s now could be this: MIS stays the cyclical torque, however MA more and more provides the bottom load. That may be a higher psychological mannequin than treating all of Moody’s as a clear read-through on company bond home windows, refinancing exercise, or unfold sentiment.

What MA’s recurring income base says about sturdiness

MA is the clearest proof that Moody’s needs to be seen by means of a broader lens. In Q1 2026, MA income elevated to $926 million from $859 million. Extra importantly, recurring income rose 11% and represented 98% of whole MA income, whereas annualized recurring income reached $3.607 billion at March 31, 2026, up from $3.343 billion a 12 months earlier. That’s the sort of income base buyers often affiliate with workflow software program, knowledge, and threat infrastructure quite than with a traditional transaction enterprise.

The stress check inside these numbers is much more revealing. MA transaction income declined 54% 12 months over 12 months in Q1 2026. In a enterprise that depended primarily on episodic challenge work, that sort of drop would possible pull the entire phase down. As a substitute, MA nonetheless grew as a result of the subscription-heavy portion of the franchise was sturdy sufficient to soak up the hit. That’s precisely what recurring income is meant to do for buyers: cut back dependence on short-term deal movement.

The sample was already seen on the finish of FY2025. MA income was about $3.6 billion for the 12 months, MA ARR was $3.498 billion at December 31, 2025 versus $3.233 billion a 12 months earlier, and MA adjusted working margin improved to 33.1%. Moody’s additionally mentioned MA recurring income comprised 97% of whole MA income in This fall 2025. That doesn’t imply MA is resistant to macro stress, competitors, or product-execution threat. It does imply that a big share of Moody’s economics now comes from recurring analytical instruments and knowledge relationships which are much less delicate to any single issuance quarter.

That recurring base additionally helps margin enchancment. MA adjusted working margin rose to 32.5% in Q1 2026 from 30.0% a 12 months earlier. For buyers, that could be a helpful sign that Moody’s is not only shopping for stability at the price of profitability. The analytics aspect is scaling.

Why MIS nonetheless drives working leverage when markets are open

None of this reduces the significance of MIS. The truth is, the rankings enterprise remains to be the primary motive Moody’s can produce outsized earnings energy in constructive markets. In Q1 2026, MIS income rose to $1.153 billion from $1.065 billion. Transaction income elevated to $790 million from $732 million, and recurring income elevated to $363 million from $333 million. That blend issues. MIS isn’t purely transaction-driven both; surveillance and associated recurring work present some continuity. However when issuance picks up, the transaction line can add high-margin income shortly.

That’s the reason the phase’s profitability is so putting. MIS adjusted working margin reached 66.7% in Q1 2026, after hitting 63.6% in FY2025. Traders don’t have to overcomplicate the takeaway: when debt markets are wholesome, MIS can convert that surroundings into very sturdy incremental earnings.

Administration’s commentary additionally reveals the place issuance demand is evolving. Moody’s mentioned Q1 2026 included file first-quarter investment-grade issuance, together with jumbo transactions and elevated AI-related financing from hyperscalers. It additionally mentioned Infrastructure Finance had its strongest quarter since 2020, helped by infrastructure funding wants and AI- and data-center-related exercise. In FY2025, Moody’s mentioned personal credit score exercise accounted for about 20% of MIS transaction income development.

These particulars shouldn’t be learn as hype factors. The extra helpful interpretation is that MIS is benefiting from a number of financing channels, not only a generic reopening in public debt markets. That broadens the chance set, even when it doesn’t eradicate cyclicality.

What buyers ought to watch subsequent: issuance high quality, regulation, and capital allocation

The principle threat to the thesis is simple: if capital markets seize up, MIS transaction income can fall sharply. Moody’s has made the consolidated mannequin extra sturdy, however it has not eliminated the cycle. That’s the reason buyers ought to watch not simply issuance quantity, however issuance combine and high quality. If present power is being supported by unusually favorable financing home windows or concentrated themes, the margin advantages in MIS might show much less sturdy than they have a look at the highest of the cycle.

Regulation stays one other actual threat. Rankings businesses function in a enterprise the place credibility, methodology, and battle administration matter as a lot as uncooked quantity. Even a well-diversified Moody’s can’t escape the potential of regulatory stress, litigation, or tighter scrutiny throughout pressured credit score durations.

Traders also needs to watch whether or not MA can maintain its present high quality of development. ARR elevated to $3.607 billion in Q1 2026, however the important thing query is whether or not that tempo can proceed whereas sustaining product relevance and wholesome retention. A recurring enterprise is sturdy provided that clients stay embedded and keen to resume.

Lastly, capital allocation deserves consideration. Moody’s returned about $1.7 billion to shareholders in Q1 2026, together with $1.5 billion in buybacks and $185 million in dividends, and it raised 2026 share repurchase steerage to about $2.5 billion from about $2.0 billion. At March 31, 2026, Moody’s had $1.469 billion in money and money equivalents, $41 million in short-term investments, and $6.387 billion in long-term debt. At year-end 2025, it had $2.384 billion in money, $64 million in short-term investments, about $7.0 billion of excellent debt, and an undrawn $1.25 billion revolving credit score facility. That isn’t a pressured stability sheet, however it does imply aggressive repurchases needs to be judged towards the identical sturdiness commonplace buyers apply to the working mannequin.

The larger image is that Moody’s now combines a recurring analytics franchise with a high-margin rankings engine. That doesn’t make it recession-proof or regulation-proof. It does make it extra sturdy than the previous one-line description of “bond-market proxy” suggests.

Key Indicators for Traders

- MA’s 98% recurring income combine in Q1 2026 suggests Moody’s has a stronger income ground than buyers often assume for a ratings-centered enterprise.

- MIS margin efficiency will stay the clearest learn on how a lot working leverage Moody’s can unlock when issuance markets keep open.

- ARR development at MA is a key sturdiness indicator; if that slows materially, the case for Moody’s as a two-engine compounder weakens.

- AI-related financing, infrastructure funding, and personal credit score are price monitoring as a result of they present the place future rankings demand might come from, not simply how a lot issuance is going on total.

- The sooner tempo of buybacks raises the significance of balance-sheet self-discipline if issuance circumstances soften.

Sources

- https://www.sec.gov/Archives/edgar/knowledge/1059556/000162828026026383/0001628280-26-026383-index.htm

- https://www.sec.gov/Archives/edgar/knowledge/1059556/000162828026026383/a1q26earningsrelease.htm

- https://www.sec.gov/Archives/edgar/knowledge/1059556/000162828026026848/mco-20260331.htm

- https://www.sec.gov/Archives/edgar/knowledge/1059556/000162828026008788/a4q25earningsrelease.htm

- https://www.sec.gov/Archives/edgar/knowledge/1059556/000162828026009136/mco-20251231.htm

All figures above are drawn from Moody’s SEC filings and official earnings releases.

{kind=link}