Picture supply: Getty Photographs

Enticing earnings shares don’t exist simply on the UK inventory market. Moderately, throughout the pond within the S&P 500, there are numerous examples of shares with excessive yields. In fact, this doesn’t imply that every one are value shopping for. Nevertheless, after I noticed one with a dividend yield of 9.8%, I made a decision it was time to dig deeper!

A shopper staples large

I’m speaking about Conagra Manufacturers (NYSE:CAG). Even in case you haven’t heard of the mother or father firm, you’ll most likely know a number of the manufacturers it owns. It’s the maker of Birds Eye greens, Wholesome Selection meals, and different meals merchandise. Over the previous 12 months, the share value has fallen by 40%, pushing the dividend yield to 9.8%.

Let’s deal with the inventory fall first. The largest challenge has been inflation. Meat, packaging, freight, and commodity prices have surged, negatively impacting profitability. Final month, a quarterly replace confirmed it expects value inflation of a whopping 7% this 12 months alone. That is being pushed partly by tariffs and rising protein costs.

On the identical time, buyers have gotten extra price-sensitive. Many customers are buying and selling all the way down to cheaper private-label alternate options as an alternative of shopping for branded frozen meals and snacks. Reported internet gross sales for the fiscal Q3 decreased by 1.9% versus the identical interval final 12 months.

Dividend enchantment

Regardless of these worries, the dividend yield does look enticing. Close to 10%, it’s terribly excessive for a shopper staples firm. Extra importantly, the corporate has paid dividends repeatedly for the reason that Nineteen Seventies.

But when assessing if the payout is sustainable, it’s a troublesome query to obviously reply. Even after latest earnings stress, Conagra continues to generate substantial money movement. For instance, within the newest quarter, it generated $896m in internet money movement. Administration has lately refinanced debt and reiterated its dedication to shareholder returns, equivalent to through dividends.

There are additionally indicators that elements of the enterprise could also be stabilising. CEO Sean Connelly stated within the newest replace that he was seeing “continued upward inflection in our Frozen and Snacks companies”. These two areas lately returned to modest natural progress. If inflation moderates and pricing stress eases, earnings might get better sooner than traders anticipate. This, in flip, would assist the dividend.

Overarching considerations

Even with the potential inexperienced shoots rising, debt stays elevated following years of acquisitions. At $7.3bn, it’s nonetheless appreciable! Additional, Walmart accounts for practically 30% of gross sales, creating main buyer focus danger. And if inflation stays stubbornly excessive with added stress from the latest power value shock, revenue margins may very well be squeezed much more.

On that foundation, I believe there are higher dividend shares that provide a extra interesting risk-to-reward ratio. I imagine this holds true each for US shares and UK alternate options. Nevertheless, traders with the next danger tolerance than me would possibly wish to contemplate it.

Picture supply: Getty Photographs

Enticing earnings shares don’t exist simply on the UK inventory market. Moderately, throughout the pond within the S&P 500, there are numerous examples of shares with excessive yields. In fact, this doesn’t imply that every one are value shopping for. Nevertheless, after I noticed one with a dividend yield of 9.8%, I made a decision it was time to dig deeper!

A shopper staples large

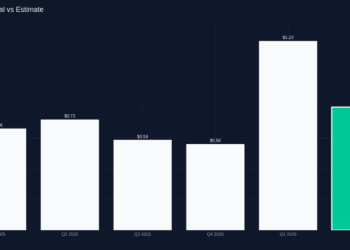

I’m speaking about Conagra Manufacturers (NYSE:CAG). Even in case you haven’t heard of the mother or father firm, you’ll most likely know a number of the manufacturers it owns. It’s the maker of Birds Eye greens, Wholesome Selection meals, and different meals merchandise. Over the previous 12 months, the share value has fallen by 40%, pushing the dividend yield to 9.8%.

Let’s deal with the inventory fall first. The largest challenge has been inflation. Meat, packaging, freight, and commodity prices have surged, negatively impacting profitability. Final month, a quarterly replace confirmed it expects value inflation of a whopping 7% this 12 months alone. That is being pushed partly by tariffs and rising protein costs.

On the identical time, buyers have gotten extra price-sensitive. Many customers are buying and selling all the way down to cheaper private-label alternate options as an alternative of shopping for branded frozen meals and snacks. Reported internet gross sales for the fiscal Q3 decreased by 1.9% versus the identical interval final 12 months.

Dividend enchantment

Regardless of these worries, the dividend yield does look enticing. Close to 10%, it’s terribly excessive for a shopper staples firm. Extra importantly, the corporate has paid dividends repeatedly for the reason that Nineteen Seventies.

But when assessing if the payout is sustainable, it’s a troublesome query to obviously reply. Even after latest earnings stress, Conagra continues to generate substantial money movement. For instance, within the newest quarter, it generated $896m in internet money movement. Administration has lately refinanced debt and reiterated its dedication to shareholder returns, equivalent to through dividends.

There are additionally indicators that elements of the enterprise could also be stabilising. CEO Sean Connelly stated within the newest replace that he was seeing “continued upward inflection in our Frozen and Snacks companies”. These two areas lately returned to modest natural progress. If inflation moderates and pricing stress eases, earnings might get better sooner than traders anticipate. This, in flip, would assist the dividend.

Overarching considerations

Even with the potential inexperienced shoots rising, debt stays elevated following years of acquisitions. At $7.3bn, it’s nonetheless appreciable! Additional, Walmart accounts for practically 30% of gross sales, creating main buyer focus danger. And if inflation stays stubbornly excessive with added stress from the latest power value shock, revenue margins may very well be squeezed much more.

On that foundation, I believe there are higher dividend shares that provide a extra interesting risk-to-reward ratio. I imagine this holds true each for US shares and UK alternate options. Nevertheless, traders with the next danger tolerance than me would possibly wish to contemplate it.

{kind=link}