Tesla (NASDAQ:TSLA) was one of many shares to outperform the S&P 500 in 2025. And that tells me rather a lot about what buyers are fascinated by the corporate proper now.

The final 12 months have been massively difficult for the enterprise. However there have been some promising indicators and the inventory market appears to be satisfied – in the intervening time.

Automobile gross sales

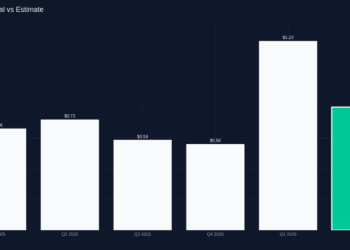

Tesla shares climbed round 19% in 2025, however this wasn’t due to larger gross sales and income. Complete revenues fell 3% throughout the first 9 months and earnings per share had been down 38%.

One purpose for this was the removing of the inexperienced vitality credit that had boosted the agency’s gross sales and income. However the information on this entrance won’t be fully unhealthy. With regards to manufacturing electrical automobiles, Tesla’s scale is unmatched. And that provides it a real price benefit over the likes of Ford and Common Motors that’s nonetheless intact.

Meaning it’s in a greater place to deal with the phasing out of credit used to incentivise producers and consumers. However there are different dangers to think about on this entrance. The most important menace to Tesla when it comes to automotive gross sales in all probability isn’t different US rivals – it’s corporations primarily based in China. And people corporations are ready to be aggressive on worth.

Lengthy story quick, it’s been a tricky 12 months for Tesla’s automobile gross sales. However buyers are keen – no less than in the intervening time – to go together with the concept it’s not likely a automotive firm.

Autonomy and robotics

The true pleasure round Tesla inventory in 2025 got here from its autonomous automobile division. The agency lastly launched its robotaxi community, which now transports actual passengers.

Automobiles at present have a human security monitor within the automotive as a result of the agency hasn’t but achieved Degree 4 autonomy underneath native laws. In that sense, it’s nonetheless behind Waymo.

If Tesla can get there although, it should have an enormous price benefit over Waymo as a result of its driverless system is less expensive to supply. And it’s nearer now than it was a 12 months in the past.

That is what’s been pushing the inventory larger. There’s an necessary sense during which the corporate might go from being behind to being miles in entrance virtually in a single day.

One space the place there’s much less competitors to cope with is robotics. Tesla missed manufacturing targets for its Optimus humanoid robotic by a good distance (roughly 1,000 vs 5,000). The corporate did nonetheless, make good progress with its know-how. And that provides buyers one thing else to deal with in 2026.

What’s going to 2026 convey?

Tesla’s outperformed in 2025 as a result of buyers are trying previous the present realities of automotive gross sales and specializing in the potential of automation. And which may nicely be justified. I believe the inventory in 2026 relies upon fully on administration’s capability to maintain them doing this. However that could be simpler mentioned than finished.

A number of shareholders say that Tesla isn’t a automotive firm. However they voted via a pay bundle for the CEO with a bonus that’s activated by promoting a sure variety of automobiles.

The inventory might undoubtedly go larger in 2026 and I’m not betting in opposition to it. By way of an funding although, there’s far an excessive amount of optimism mirrored within the share worth for my liking.

Tesla (NASDAQ:TSLA) was one of many shares to outperform the S&P 500 in 2025. And that tells me rather a lot about what buyers are fascinated by the corporate proper now.

The final 12 months have been massively difficult for the enterprise. However there have been some promising indicators and the inventory market appears to be satisfied – in the intervening time.

Automobile gross sales

Tesla shares climbed round 19% in 2025, however this wasn’t due to larger gross sales and income. Complete revenues fell 3% throughout the first 9 months and earnings per share had been down 38%.

One purpose for this was the removing of the inexperienced vitality credit that had boosted the agency’s gross sales and income. However the information on this entrance won’t be fully unhealthy. With regards to manufacturing electrical automobiles, Tesla’s scale is unmatched. And that provides it a real price benefit over the likes of Ford and Common Motors that’s nonetheless intact.

Meaning it’s in a greater place to deal with the phasing out of credit used to incentivise producers and consumers. However there are different dangers to think about on this entrance. The most important menace to Tesla when it comes to automotive gross sales in all probability isn’t different US rivals – it’s corporations primarily based in China. And people corporations are ready to be aggressive on worth.

Lengthy story quick, it’s been a tricky 12 months for Tesla’s automobile gross sales. However buyers are keen – no less than in the intervening time – to go together with the concept it’s not likely a automotive firm.

Autonomy and robotics

The true pleasure round Tesla inventory in 2025 got here from its autonomous automobile division. The agency lastly launched its robotaxi community, which now transports actual passengers.

Automobiles at present have a human security monitor within the automotive as a result of the agency hasn’t but achieved Degree 4 autonomy underneath native laws. In that sense, it’s nonetheless behind Waymo.

If Tesla can get there although, it should have an enormous price benefit over Waymo as a result of its driverless system is less expensive to supply. And it’s nearer now than it was a 12 months in the past.

That is what’s been pushing the inventory larger. There’s an necessary sense during which the corporate might go from being behind to being miles in entrance virtually in a single day.

One space the place there’s much less competitors to cope with is robotics. Tesla missed manufacturing targets for its Optimus humanoid robotic by a good distance (roughly 1,000 vs 5,000). The corporate did nonetheless, make good progress with its know-how. And that provides buyers one thing else to deal with in 2026.

What’s going to 2026 convey?

Tesla’s outperformed in 2025 as a result of buyers are trying previous the present realities of automotive gross sales and specializing in the potential of automation. And which may nicely be justified. I believe the inventory in 2026 relies upon fully on administration’s capability to maintain them doing this. However that could be simpler mentioned than finished.

A number of shareholders say that Tesla isn’t a automotive firm. However they voted via a pay bundle for the CEO with a bonus that’s activated by promoting a sure variety of automobiles.

The inventory might undoubtedly go larger in 2026 and I’m not betting in opposition to it. By way of an funding although, there’s far an excessive amount of optimism mirrored within the share worth for my liking.

{kind=link}