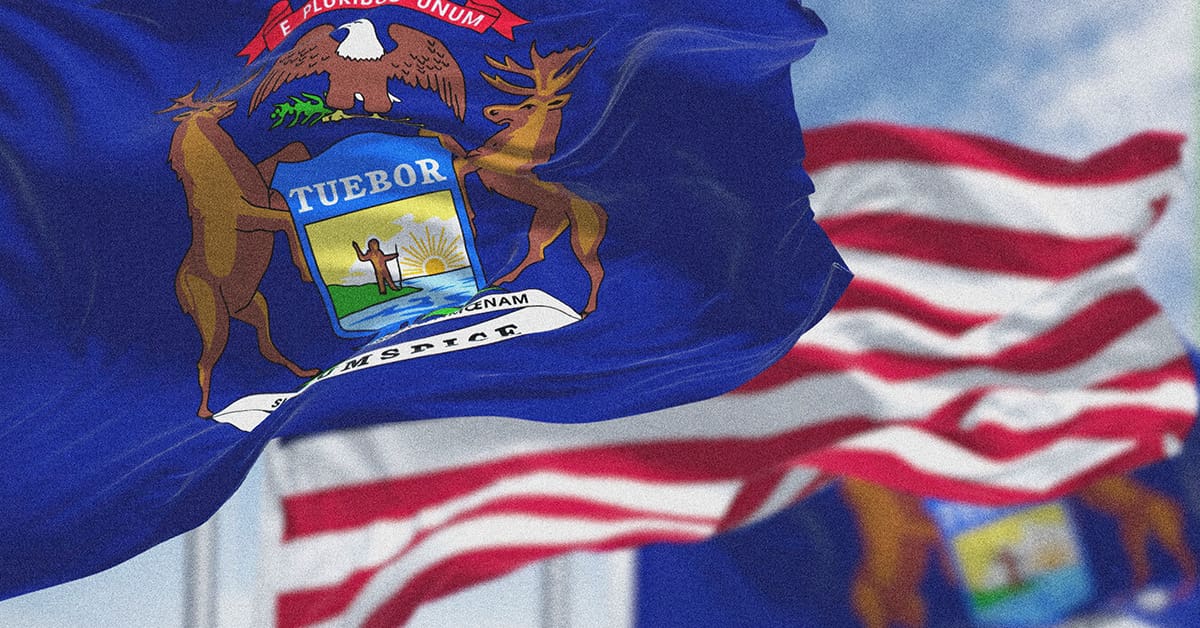

Whereas companies nationwide have been optimizing operations to benefit from the One Huge Lovely Invoice’s provisions on analysis and experimentation bills, bonus depreciation and asset expensing, Michigan companies face a special actuality. Loni Winkler of UHY explains how Gov. Gretchen Whitmer’s signing of Home Invoice 4961 decoupled Michigan from 5 federal OBBB provisions to guard state tax income, creating an estimated $520 million tax improve for enterprise house owners in 2025 as they navigate divergent federal and state guidelines on every part from bonus depreciation to enterprise curiosity deductions.

Reshaping every part from the way in which companies put money into analysis and experimentation (R&E) bonus depreciation and a number of other provisions for people, few items of laws have generated extra waves on this planet of economic coverage than the One Huge Lovely Invoice (OBBB). And given how sprawling the OBBB is, companies and their monetary and compliance groups have been onerous at work attempting to make it possible for they’re optimizing their companies to each benefit from these provisions and meet compliance expectations heading into 2026.

Nevertheless, for companies in Michigan, this just lately turned a bit tougher. In early October, Gov. Gretchen Whitmer signed the fiscal yr 2026 state price range, together with Home Invoice 4961, into regulation. This laws decouples Michigan from a number of provisions of the federal OBBB, together with:

- Fast deduction of analysis and experimental bills: IRC §174A

- Particular depreciation of sure manufacturing property: IRC §168(n)

- Bonus depreciation permitting for deduction of 100% of the price of tools within the first yr: IRC §168(okay)

- Enterprise curiosity deduction improve: IRC §163(j)

- Elevated restrict on depreciable enterprise belongings deduction: IRC §179

The first purpose for decoupling was to guard state tax income and keep away from a price range shortfall. It was estimated that conforming to OBBB would lead to a lack of about $600 million in income within the first fiscal yr, and over $2 billion via 2030. The choice was strongly protested by Michigan companies {and professional} organizations, which mentioned decoupling would quantity to a everlasting tax improve on Michigan companies. Michigan’s home fiscal company has estimated that decoupling will price enterprise house owners $520 million in elevated taxes in 2025.

What do these strikes imply for Michigan companies and their finance and compliance groups? And what issues ought to companies in different states contemplating decoupling do to organize?

Common results on computing Michigan earnings tax

Most states use the Inside Income Code (IRC) as the idea for his or her particular person and company earnings tax codes. When a state “decouples” from a particular federal tax regulation provision, this implies the state has chosen to deviate from that particular provision when figuring out its state taxable earnings. Michigan is a “rolling conformity” state in that it routinely conforms to modifications made to federal tax legal guidelines except the state particularly passes laws decoupling from the federal modifications. The decoupling provisions handed have an effect on company and pass-through entities in figuring out the earnings taxable in Michigan.

Michigan’s H.B. 4961 states that for tax years starting after Dec. 31, 2024, taxpayers should calculate their taxable earnings for Michigan as if each of the next circumstances utilized:

- Sections 168(okay), 168(n) and 174A of the IRC weren’t in impact.

- Sections 163(j), 174, and 179 of the IRC utilized per the provisions in impact Dec. 31, 2024.

As mentioned under, there’s a slight deviation between company and non-corporate taxpayers associated to the bonus depreciation (Sec. 168(okay)) guidelines.

How decoupling impacts particular provisions

For enterprise house owners, one of many standout provisions from the OBBBA was the modifications to bonus depreciation. OBBB permits 100% bonus depreciation on the federal stage, which allows companies to deduct the prices of sure belongings instantly as a substitute of over time for certified property acquired and positioned in service after Jan. 19, 2025. The Michigan’s decoupling creates completely different guidelines for bonus depreciation based mostly on the kind of taxpayer:

- For company taxpayers, the laws doesn’t enable any bonus depreciation. Accordingly, taxpayers might be required so as to add again any bonus depreciation claimed on the Federal stage.

- Non-corporate taxpayers are eligible to assert bonus depreciation, however per Federal charges previous to the passage of the OBBB: 40% in 2025, 20% in 2026 and 0% in 2027.

The OBBB additionally permits a 100% particular deduction for sure certified manufacturing property positioned in service earlier than Jan. 1, 2031, and is of explicit curiosity for areas which might be at the moment manufacturing facilities or need to increase their manufacturing sectors sooner or later. Particular steering remains to be wanted for this deduction, however basically, it would enable taxpayers to instantly depreciate buildings used to fabricate or course of merchandise in the US. Nevertheless, underneath Michigan’s invoice, companies might be required so as to add again any of the particular depreciation deduction when calculating their Michigan taxable earnings.

Beneath the Tax Cuts and Jobs Act (TCJA) enacted throughout the first Trump Administration in 2017, companies have been required to capitalize home and international analysis and experimental bills over 5 years for home bills and 15 years for international. The OBBB permits for a direct deduction on any home R&E expenditures which might be paid or incurred by a taxpayer throughout the taxable yr starting after Dec. 31, 2024. The brand new decoupling laws in Michigan requires taxpayers to proceed to capitalize and amortize R&E bills per earlier federal guidelines.

Beneath the TCJA, most companies noticed the quantity of enterprise curiosity expense restricted to 30% of their adjusted taxable earnings (ATI) via modifications to Part 163(j) of the IRC. The OBBB made everlasting a modified calculation of ATI to incorporate an addback of depreciation, amortization or depletion — thus seemingly elevating the quantity of deductible curiosity for many companies — for taxable years starting after Dec. 31, 2024. As a result of H.B. 4961 states that Part 163(j) should be utilized because it was in impact Dec. 31, 2024, Michigan companies should embrace depreciation and amortization deductions when calculating ATI. This may lead to a decrease ATI and should lead to a decrease enterprise curiosity deduction.

The OBBB elevated the restrict for expensing sure depreciable enterprise belongings. Beneath the OBBB, the restrict was elevated to $2.5 million, up from $1.22 million in 2024, for property positioned in service in taxable years starting after Dec. 31, 2024. Nevertheless, Michigan regulation is not going to observe this improve and can enable expensing solely as much as the 2024 restrict.

Begin planning now

Regardless of decoupling from a number of federal provisions, these modifications could considerably influence year-end tax planning and any estimated funds due within the subsequent two months. Correct planning can assist alleviate a few of the burden and assist keep away from tax surprises and underpayment penalties within the spring.

Whereas companies nationwide have been optimizing operations to benefit from the One Huge Lovely Invoice’s provisions on analysis and experimentation bills, bonus depreciation and asset expensing, Michigan companies face a special actuality. Loni Winkler of UHY explains how Gov. Gretchen Whitmer’s signing of Home Invoice 4961 decoupled Michigan from 5 federal OBBB provisions to guard state tax income, creating an estimated $520 million tax improve for enterprise house owners in 2025 as they navigate divergent federal and state guidelines on every part from bonus depreciation to enterprise curiosity deductions.

Reshaping every part from the way in which companies put money into analysis and experimentation (R&E) bonus depreciation and a number of other provisions for people, few items of laws have generated extra waves on this planet of economic coverage than the One Huge Lovely Invoice (OBBB). And given how sprawling the OBBB is, companies and their monetary and compliance groups have been onerous at work attempting to make it possible for they’re optimizing their companies to each benefit from these provisions and meet compliance expectations heading into 2026.

Nevertheless, for companies in Michigan, this just lately turned a bit tougher. In early October, Gov. Gretchen Whitmer signed the fiscal yr 2026 state price range, together with Home Invoice 4961, into regulation. This laws decouples Michigan from a number of provisions of the federal OBBB, together with:

- Fast deduction of analysis and experimental bills: IRC §174A

- Particular depreciation of sure manufacturing property: IRC §168(n)

- Bonus depreciation permitting for deduction of 100% of the price of tools within the first yr: IRC §168(okay)

- Enterprise curiosity deduction improve: IRC §163(j)

- Elevated restrict on depreciable enterprise belongings deduction: IRC §179

The first purpose for decoupling was to guard state tax income and keep away from a price range shortfall. It was estimated that conforming to OBBB would lead to a lack of about $600 million in income within the first fiscal yr, and over $2 billion via 2030. The choice was strongly protested by Michigan companies {and professional} organizations, which mentioned decoupling would quantity to a everlasting tax improve on Michigan companies. Michigan’s home fiscal company has estimated that decoupling will price enterprise house owners $520 million in elevated taxes in 2025.

What do these strikes imply for Michigan companies and their finance and compliance groups? And what issues ought to companies in different states contemplating decoupling do to organize?

Common results on computing Michigan earnings tax

Most states use the Inside Income Code (IRC) as the idea for his or her particular person and company earnings tax codes. When a state “decouples” from a particular federal tax regulation provision, this implies the state has chosen to deviate from that particular provision when figuring out its state taxable earnings. Michigan is a “rolling conformity” state in that it routinely conforms to modifications made to federal tax legal guidelines except the state particularly passes laws decoupling from the federal modifications. The decoupling provisions handed have an effect on company and pass-through entities in figuring out the earnings taxable in Michigan.

Michigan’s H.B. 4961 states that for tax years starting after Dec. 31, 2024, taxpayers should calculate their taxable earnings for Michigan as if each of the next circumstances utilized:

- Sections 168(okay), 168(n) and 174A of the IRC weren’t in impact.

- Sections 163(j), 174, and 179 of the IRC utilized per the provisions in impact Dec. 31, 2024.

As mentioned under, there’s a slight deviation between company and non-corporate taxpayers associated to the bonus depreciation (Sec. 168(okay)) guidelines.

How decoupling impacts particular provisions

For enterprise house owners, one of many standout provisions from the OBBBA was the modifications to bonus depreciation. OBBB permits 100% bonus depreciation on the federal stage, which allows companies to deduct the prices of sure belongings instantly as a substitute of over time for certified property acquired and positioned in service after Jan. 19, 2025. The Michigan’s decoupling creates completely different guidelines for bonus depreciation based mostly on the kind of taxpayer:

- For company taxpayers, the laws doesn’t enable any bonus depreciation. Accordingly, taxpayers might be required so as to add again any bonus depreciation claimed on the Federal stage.

- Non-corporate taxpayers are eligible to assert bonus depreciation, however per Federal charges previous to the passage of the OBBB: 40% in 2025, 20% in 2026 and 0% in 2027.

The OBBB additionally permits a 100% particular deduction for sure certified manufacturing property positioned in service earlier than Jan. 1, 2031, and is of explicit curiosity for areas which might be at the moment manufacturing facilities or need to increase their manufacturing sectors sooner or later. Particular steering remains to be wanted for this deduction, however basically, it would enable taxpayers to instantly depreciate buildings used to fabricate or course of merchandise in the US. Nevertheless, underneath Michigan’s invoice, companies might be required so as to add again any of the particular depreciation deduction when calculating their Michigan taxable earnings.

Beneath the Tax Cuts and Jobs Act (TCJA) enacted throughout the first Trump Administration in 2017, companies have been required to capitalize home and international analysis and experimental bills over 5 years for home bills and 15 years for international. The OBBB permits for a direct deduction on any home R&E expenditures which might be paid or incurred by a taxpayer throughout the taxable yr starting after Dec. 31, 2024. The brand new decoupling laws in Michigan requires taxpayers to proceed to capitalize and amortize R&E bills per earlier federal guidelines.

Beneath the TCJA, most companies noticed the quantity of enterprise curiosity expense restricted to 30% of their adjusted taxable earnings (ATI) via modifications to Part 163(j) of the IRC. The OBBB made everlasting a modified calculation of ATI to incorporate an addback of depreciation, amortization or depletion — thus seemingly elevating the quantity of deductible curiosity for many companies — for taxable years starting after Dec. 31, 2024. As a result of H.B. 4961 states that Part 163(j) should be utilized because it was in impact Dec. 31, 2024, Michigan companies should embrace depreciation and amortization deductions when calculating ATI. This may lead to a decrease ATI and should lead to a decrease enterprise curiosity deduction.

The OBBB elevated the restrict for expensing sure depreciable enterprise belongings. Beneath the OBBB, the restrict was elevated to $2.5 million, up from $1.22 million in 2024, for property positioned in service in taxable years starting after Dec. 31, 2024. Nevertheless, Michigan regulation is not going to observe this improve and can enable expensing solely as much as the 2024 restrict.

Begin planning now

Regardless of decoupling from a number of federal provisions, these modifications could considerably influence year-end tax planning and any estimated funds due within the subsequent two months. Correct planning can assist alleviate a few of the burden and assist keep away from tax surprises and underpayment penalties within the spring.

{kind=link}